September 29, 2018 (LBO) - The main subject of discussion on the Colombo cocktail circuit has been the Sri Lanka Rupee (LKR) and its significant recent weakness against the U.S. dollar (USD). The LKR seems to have halted its slide, hovering just under Rs170 to the dollar.

This recent price stability in the LKR is not due to the fundamentals stabilising, but rather due to intervention by the Central Bank of Sri Lanka (CBSL) in the currency markets. Last week Senior Deputy Governor Nandalal Weerasinghe said the Central Bank will intervene aggressively to curb excess volatility in the exchange rate.

These statements and subsequent intervention have come amidst a backdrop of aggressive political rhetoric critical of the government's management of the economy and its currency. There have been some statements, one in particular by Finance Minister Mangala Samaraweera, saying the interventions to prop up the rupee are unsustainable. To date, the Governor of the CBSL and the Monetary Board he chairs have yet to make definitive statements on the slide in rupee or policy on intervention in the currency markets.

Some politicians like State Minister of Economic Affairs Harsha De Silva have opined that Sri Lankans should accept austerity and curb their consumption of items which cause a drain on foreign currency like automobile purchases or foreign travel. The minister has been highly criticised for these statements as the public are well aware of the corrupt and luxurious lives of many of the country's political leaders. Some have compared these comments to those of Turkish President Erdogan who has urged his people to convert their dollars to lira as a show of patriotism. These comments in Turkey have exacerbated the problem causing an even greater demand for foreign currency.

Exacerbating the problem seems to be what is now happening in Sri Lanka. Up until recently, the CBSL and its Governor have preserved the nation's foreign reserves by allowing the rupee to depreciate in line with market forces.

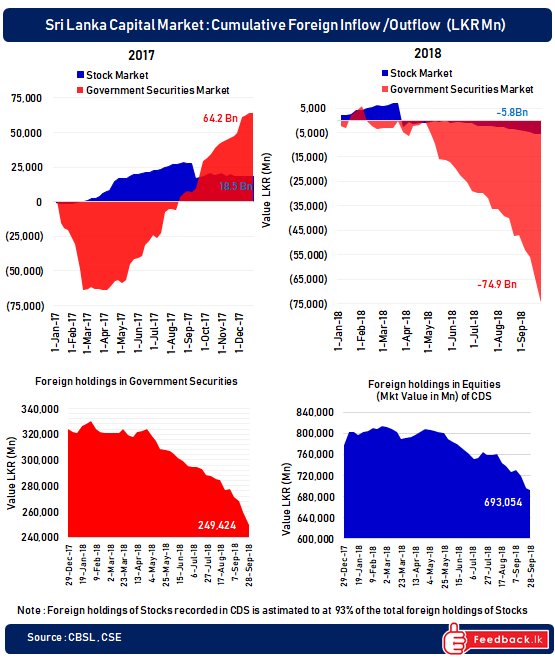

However, now the CBSL is intervening and currency reserves and being depleted at a rapid rate. Exactly how fast they are being drawn down is not known by the marketplace at this juncture. This intervention has artificially kept the rupee just under 170 to the dollar, and it appears the foreign investors in Sri Lanka's government securities are taking advantage of it.

Selling by foreigners of Sri Lankan bonds has accelerated, and it appears that they are using CBSL intervention in the currency markets to get out with out pushing down the currency.

buy amoxil online

buy amoxil online no prescription

This year Rs75bn of net foreign selling has hit the Sri Lankan bond markets with recent weeks seeing outflows increasing to as much as Rs10bn.

It is important for the CBSL to understand basic investor behaviour. If holders of Sri Lankan government securities know that the CBSL is intervening at an unsustainable pace, they will take advantage of the intervention to exit ahead of an inevitable significant devaluation. The intervention intended to prop up the LKR is likely exacerbating the selling of government securities by foreigners which will cause the fundamentals of the currency to deteriorate even further. The same phenomenon to a lesser degree is also likely to happen in the Colombo Stock Market.

The recent currency pressure has certainly been a global phenomenon. The CBSL of Sri Lanka is too small an institution to fight this trend. Up until now, Governor Indrajit Coomaraswamy has conducted an impressive textbook monetary policy that has enabled the nation to preserve its foreign reserves. Let us hope that political pressure to prop up the LKR does not force the Governor to squander the unprecedented level of credibility he has established for the CBSL to date. He is certainly the best official the Sri Lanka government has, and I would encourage him not to bow to the political rhetoric from those whose understanding of monetary policy is limited.

Image courtesy of Sanjeewa Dayarathne