A summary of the performance of the Sri Lankan economy in 2018 as reflected in the Annual Report is given below:

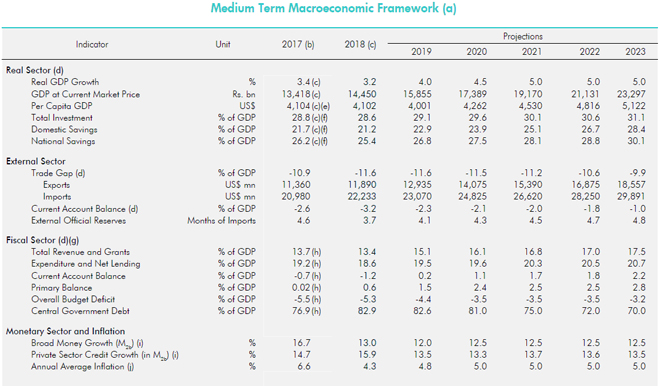

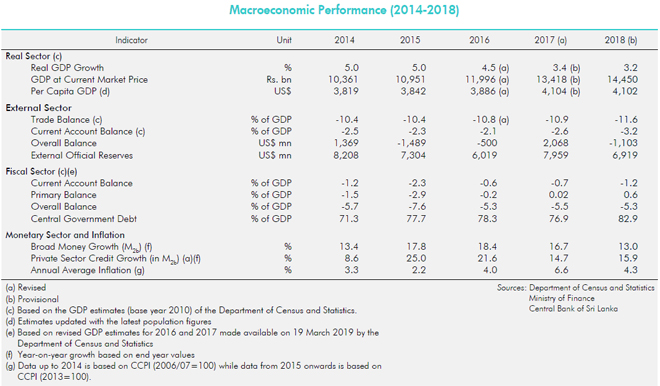

The vulnerability of the Sri Lankan economy to global and domestic disturbances became increasingly visible in 2018, with a modest expansion in real economic activity amidst a low inflation environment during the year. Real GDP growth was recorded at 3.2 per cent in 2018, compared to 3.4 per cent in the previous year. This growth was largely supported by services activities that expanded by 4.7 per cent and the recovery in agriculture activities, which recorded a growth of 4.8 per cent. Industry activities slowed down significantly to 0.9 per cent during the year, mainly as a result of the contraction in construction. According to the expenditure approach, both consumption and investment expenditure supported growth. Investment as a percentage of GDP stood at 28.6 per cent in 2018 compared to 28.8 per cent in the previous year, while the savings-investment gap widened during the year indicating increased dependence on external resources to fill the shortfall. The total size of the Sri Lankan economy was estimated at US dollars 88.9 billion, while the per capita GDP was recorded at US dollars 4,102 in 2018, which was marginally lower than in the previous year. Amidst the moderate growth in economic activity, a marginal increase in the unemployment rate and a decline in the labour force participation rate were observed during the year.

The external sector of the economy was volatile during the year due to both global and domestic factors. Globally, monetary policy normalisation, particularly in the United States of America (USA), resulted in global financial conditions tightening, thus causing capital outflows from emerging market economies and increased pressure on exchange rates of twin deficit economies, in particular. Sri Lanka also experienced these headwinds, particularly from mid-April 2018, which were exacerbated following the political uncertainties and the downgrade of the country’s Sovereign rating in the fourth quarter of the year. Domestically, the trade deficit surpassed US dollars 10 billion for the first time in history with higher growth in import expenditure outpacing the growth in export earnings, which were at a record level in nominal terms. Although services exports are estimated to have grown substantially, the deficit in the merchandise trade balance, stagnant workers’ remittances and rising foreign interest payments resulted in a widened current account deficit of 3.2 per cent of GDP during the year. The financial account benefitted from increased foreign direct investment (FDI) inflows which recorded its historically highest level in 2018, as well as borrowing from abroad, particularly through the issuance of International Sovereign Bonds (ISBs). The combined result of these developments was a deficit in the overall balance in the balance of payments (BOP). In 2018, the Central Bank followed a market based exchange rate policy and allowed a sharper depreciation of the rupee, but intervened in the domestic foreign exchange market, particularly at times when large capital outflows and undue speculation caused excessive volatility in the market. In order to address the widening trade deficit, the Central Bank and the government implemented a series of measures to curb non-essential imports by increasing tariffs, imposing margin requirements, tightening loan-to-value ratios on selected types of lending, and suspending the issuance of letters of credit (LCs) on concessionary permits for vehicle imports. In response to these measures and the global financial markets becoming less unfavourable, the pressure on the BOP and the exchange rate subsided during late 2018 and early 2019, and the Sri Lankan rupee appreciated against major currencies during the first quarter of 2019, thus correcting the overshooting of the exchange rate observed in the previous year to some extent. The resumption of discussions and the achievement of staff level agreement with the International Monetary Fund (IMF) on the programme under the Extended Fund Facility (EFF) arrangement in February 2019 also helped improve investor sentiments.

In spite of the sharp depreciation of the rupee and the introduction of the pricing formula for domestic petroleum price adjustments, headline and core inflation remained well anchored in low single digit levels during the year, supported by proactive monetary policy measures, improved domestic supply conditions, and also due to subdued aggregate demand conditions. Headline inflation fluctuated largely in line with the price movements of the food category, where food prices declined mostly during 2018 owing to favourable weather conditions that prevailed during the year. Inflation is expected to remain well within mid single digit levels in the medium term, particularly under the envisaged flexible inflation targeting (FIT) regime. Subdued inflation and inflation expectations and lower than potential growth in real economic activity prompted the Central Bank to signal an end to the monetary tightening cycle in April 2018 by reducing the Standing Lending Facility Rate (SLFR) by 25 basis points. Thereafter, the Central Bank maintained a neutral monetary policy stance throughout the year, in view of the continued pressure on the external sector amidst the subpar performance in the domestic economy. Nevertheless, the large and persistent liquidity deficit in the domestic money market, particularly since September 2018, compelled the Central Bank to inject liquidity on a permanent basis in November 2018, by way of reducing the Statutory Reserve Ratio (SRR) applicable on all rupee deposit liabilities of commercial banks by 1.50 percentage points. However, at the same time, to neutralise the impact of the SRR reduction and maintain its neutral policy stance, the Central Bank increased the Standing Deposit Facility Rate (SDFR) by 75 basis points and SLFR by 50 basis points, further narrowing the policy rate corridor to 100 basis points. Accordingly, by end 2018, SDFR and SLFR stood at 8.00 per cent and 9.00 per cent, respectively. As the shortage in rupee liquidity persisted into early 2019, the Central Bank reduced the SRR by a further 1.00 percentage point to 5.00 per cent effective 01 March 2019. Meanwhile, the year-on-year growth of broad money (M2b) decelerated in 2018 driven by the contraction in net foreign assets (NFA) of the banking sector. However, within broad money growth, the overall expansion of credit granted to the private sector by commercial banks in 2018 was higher than expected, in spite of tight liquidity conditions and high nominal and real market interest rates.

In the meantime, fiscal operations during 2018 demonstrated some improvements with a higher primary surplus and a lower budget deficit, notwithstanding the decline in revenue mobilisation. The government revenue declined to 13.3 per cent of GDP in 2018 while expenditure and net lending declined, particularly due to lower public investment, which was affected by political tensions that prevailed towards the end of the year resulting in delays in the implementation of budgetary operations. Reduced capital expenditure also contributed to a dampening of economic activity. The current account deficit increased in 2018 as a percentage of GDP reflecting dissavings of the government. The primary balance, which mirrors the difference between the government revenue and non-interest expenditure, registered a surplus of 0.

A summary of the performance of the Sri Lankan economy in 2018 as reflected in the Annual Report is given below:

The vulnerability of the Sri Lankan economy to global and domestic disturbances became increasingly visible in 2018, with a modest expansion in real economic activity amidst a low inflation environment during the year. Real GDP growth was recorded at 3.2 per cent in 2018, compared to 3.4 per cent in the previous year. This growth was largely supported by services activities that expanded by 4.7 per cent and the recovery in agriculture activities, which recorded a growth of 4.8 per cent. Industry activities slowed down significantly to 0.9 per cent during the year, mainly as a result of the contraction in construction. According to the expenditure approach, both consumption and investment expenditure supported growth. Investment as a percentage of GDP stood at 28.6 per cent in 2018 compared to 28.8 per cent in the previous year, while the savings-investment gap widened during the year indicating increased dependence on external resources to fill the shortfall. The total size of the Sri Lankan economy was estimated at US dollars 88.9 billion, while the per capita GDP was recorded at US dollars 4,102 in 2018, which was marginally lower than in the previous year. Amidst the moderate growth in economic activity, a marginal increase in the unemployment rate and a decline in the labour force participation rate were observed during the year.

The external sector of the economy was volatile during the year due to both global and domestic factors. Globally, monetary policy normalisation, particularly in the United States of America (USA), resulted in global financial conditions tightening, thus causing capital outflows from emerging market economies and increased pressure on exchange rates of twin deficit economies, in particular. Sri Lanka also experienced these headwinds, particularly from mid-April 2018, which were exacerbated following the political uncertainties and the downgrade of the country’s Sovereign rating in the fourth quarter of the year. Domestically, the trade deficit surpassed US dollars 10 billion for the first time in history with higher growth in import expenditure outpacing the growth in export earnings, which were at a record level in nominal terms. Although services exports are estimated to have grown substantially, the deficit in the merchandise trade balance, stagnant workers’ remittances and rising foreign interest payments resulted in a widened current account deficit of 3.2 per cent of GDP during the year. The financial account benefitted from increased foreign direct investment (FDI) inflows which recorded its historically highest level in 2018, as well as borrowing from abroad, particularly through the issuance of International Sovereign Bonds (ISBs). The combined result of these developments was a deficit in the overall balance in the balance of payments (BOP). In 2018, the Central Bank followed a market based exchange rate policy and allowed a sharper depreciation of the rupee, but intervened in the domestic foreign exchange market, particularly at times when large capital outflows and undue speculation caused excessive volatility in the market. In order to address the widening trade deficit, the Central Bank and the government implemented a series of measures to curb non-essential imports by increasing tariffs, imposing margin requirements, tightening loan-to-value ratios on selected types of lending, and suspending the issuance of letters of credit (LCs) on concessionary permits for vehicle imports. In response to these measures and the global financial markets becoming less unfavourable, the pressure on the BOP and the exchange rate subsided during late 2018 and early 2019, and the Sri Lankan rupee appreciated against major currencies during the first quarter of 2019, thus correcting the overshooting of the exchange rate observed in the previous year to some extent. The resumption of discussions and the achievement of staff level agreement with the International Monetary Fund (IMF) on the programme under the Extended Fund Facility (EFF) arrangement in February 2019 also helped improve investor sentiments.

In spite of the sharp depreciation of the rupee and the introduction of the pricing formula for domestic petroleum price adjustments, headline and core inflation remained well anchored in low single digit levels during the year, supported by proactive monetary policy measures, improved domestic supply conditions, and also due to subdued aggregate demand conditions. Headline inflation fluctuated largely in line with the price movements of the food category, where food prices declined mostly during 2018 owing to favourable weather conditions that prevailed during the year. Inflation is expected to remain well within mid single digit levels in the medium term, particularly under the envisaged flexible inflation targeting (FIT) regime. Subdued inflation and inflation expectations and lower than potential growth in real economic activity prompted the Central Bank to signal an end to the monetary tightening cycle in April 2018 by reducing the Standing Lending Facility Rate (SLFR) by 25 basis points. Thereafter, the Central Bank maintained a neutral monetary policy stance throughout the year, in view of the continued pressure on the external sector amidst the subpar performance in the domestic economy. Nevertheless, the large and persistent liquidity deficit in the domestic money market, particularly since September 2018, compelled the Central Bank to inject liquidity on a permanent basis in November 2018, by way of reducing the Statutory Reserve Ratio (SRR) applicable on all rupee deposit liabilities of commercial banks by 1.50 percentage points. However, at the same time, to neutralise the impact of the SRR reduction and maintain its neutral policy stance, the Central Bank increased the Standing Deposit Facility Rate (SDFR) by 75 basis points and SLFR by 50 basis points, further narrowing the policy rate corridor to 100 basis points. Accordingly, by end 2018, SDFR and SLFR stood at 8.00 per cent and 9.00 per cent, respectively. As the shortage in rupee liquidity persisted into early 2019, the Central Bank reduced the SRR by a further 1.00 percentage point to 5.00 per cent effective 01 March 2019. Meanwhile, the year-on-year growth of broad money (M2b) decelerated in 2018 driven by the contraction in net foreign assets (NFA) of the banking sector. However, within broad money growth, the overall expansion of credit granted to the private sector by commercial banks in 2018 was higher than expected, in spite of tight liquidity conditions and high nominal and real market interest rates.

In the meantime, fiscal operations during 2018 demonstrated some improvements with a higher primary surplus and a lower budget deficit, notwithstanding the decline in revenue mobilisation. The government revenue declined to 13.3 per cent of GDP in 2018 while expenditure and net lending declined, particularly due to lower public investment, which was affected by political tensions that prevailed towards the end of the year resulting in delays in the implementation of budgetary operations. Reduced capital expenditure also contributed to a dampening of economic activity. The current account deficit increased in 2018 as a percentage of GDP reflecting dissavings of the government. The primary balance, which mirrors the difference between the government revenue and non-interest expenditure, registered a surplus of 0.buy singulair online buy singulair online no prescription

6 per cent of GDP in 2018 compared to the surplus of 0.02 per cent of GDP in 2017. The budget deficit declined to 5.3 per cent of GDP in 2018 from 5.5 per cent of GDP in 2017 as a result of the substantial reduction in capital expenditure, but a deviation from the target level of 4.8 per cent of GDP envisaged in the Budget 2018 was also observed. The outstanding central government debt increased to 82.9 per cent of GDP at end 2018 from 76.9 per cent at end 2017, which is attributed to the depreciation of the rupee that affected the rupee value of foreign debt, relatively low nominal GDP and higher net borrowings during the period. Rollover risks can be contained through the implementation of the provisions of the Active Liability Management Act (ALMA) and the introduction of the Medium Term Debt Management Strategy (MTDS), which would help manage the government’s debt obligations in the period ahead, with the support of continued commitment towards revenue based fiscal consolidation. The financial sector continued to expand in 2018, supported by the moderate but stable growth of the banking sector. However, the profitability of the banking sector declined during the year mainly due to some deterioration in the asset quality, a rise in operating costs and higher taxes. The Central Bank strengthened the prudential policy measures, including the implementation of Basel III requirements and the adoption of Sri Lanka Accounting Standard - SLFRS 9 during the year. Meanwhile, the Licensed Finance Companies (LFCs) and Specialised Leasing Companies (SLCs) sector also recorded moderate growth amidst a challenging environment, and the Central Bank took measures to resolve distressed finance companies and to address the lingering concerns in the sector. The Colombo Stock Exchange (CSE) recorded yet another year of poor performance due to adverse developments on domestic and global fronts, which affected investor sentiments. Amidst efforts to maintain the country’s macroeconomic stability over the past several years, the postponement of much needed structural reforms has moved the Sri Lankan economy to a modest growth path. Sri Lanka’s graduation to the middle income status almost a decade ago required far reaching policy reforms to move towards higher income status by avoiding the so-called middle income trap. However, delays in addressing barriers to growth and introducing growth enhancing reforms in the areas of export promotion, attracting FDI, reducing budget deficits and debt levels, reforming factor markets, strengthening public administration, and ensuring the rule of law have largely contributed to Sri Lanka’s economic stagnation, while peer economies have progressed rapidly as a result of growth supporting reforms. Therefore, for Sri Lanka to succeed as a higher income economy and improve the wellbeing of its people, it is essential that the root causes for the continued low economic growth are addressed by expediting the required structural reforms with a focus on improving productivity and efficiency of the economy. In this background, it is vital that all stakeholders make concerted efforts to expedite the reform agenda that is already in place, which includes the National Export Strategy (NES) and New Trade Policy (NTP) to improve earnings from merchandise and service exports, the fiscal consolidation programme to improve fiscal discipline and debt sustainability, and the Central Bank’s move towards adopting FIT by 2020 to ensure sustained price stability. The timely implementation of these reforms will not only improve Sri Lanka’s economic outlook and its prospects as a highly sought after destination for investments given the country’s strategic location in the Indian Ocean, but also would be essential to uplift the overall standard of living and quality of life of its people.The country can no longer afford to postpone such reforms, if Sri Lanka is to progress along a high and sustainable growth trajectory over the medium term and catch up with countries that were behind Sri Lanka several decades ago.