By PwC Sri Lanka

The Nexus between Property and Road Development in Sri Lanka

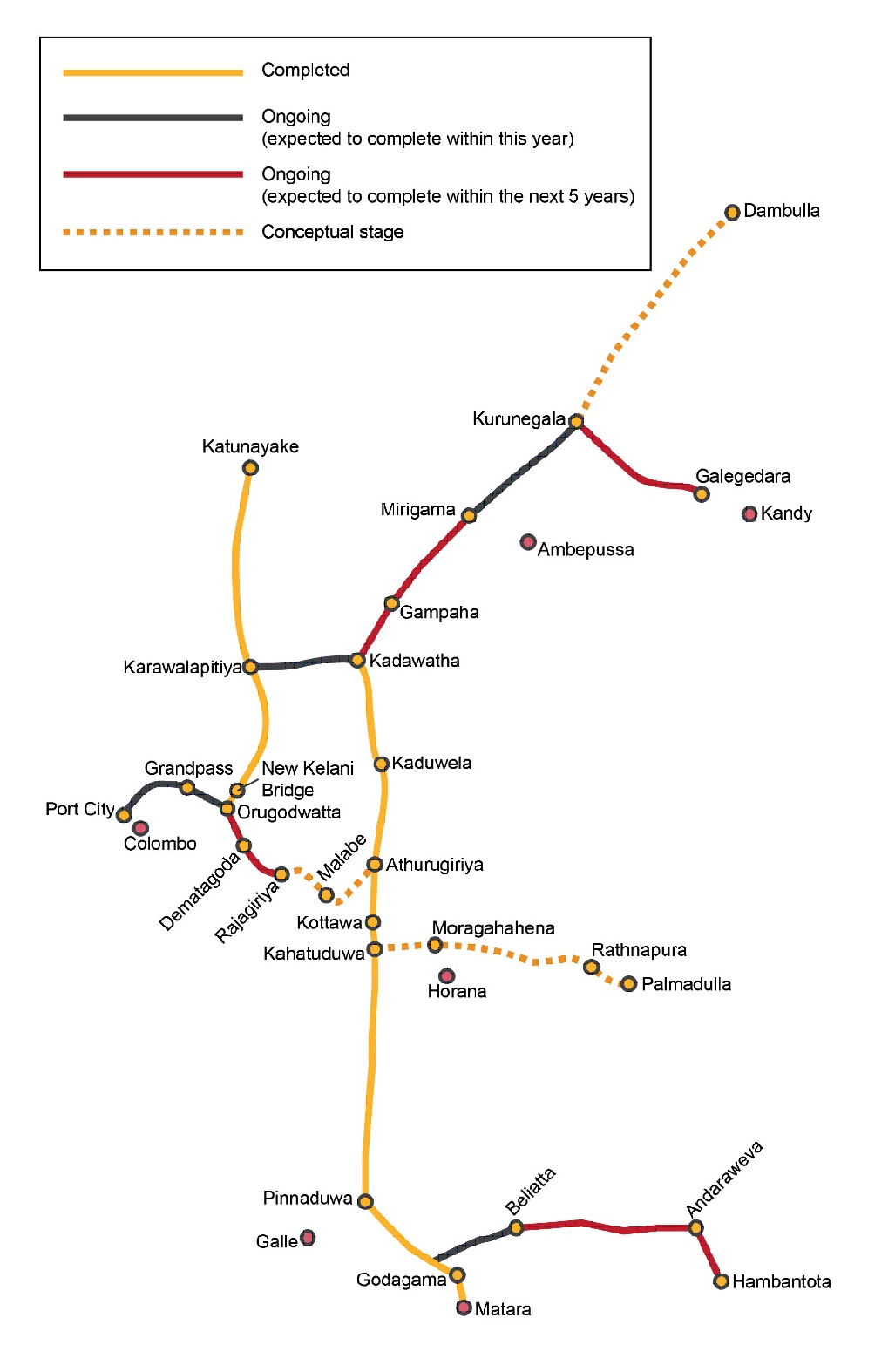

Post war Sri Lanka has seen a dramatic revival to its infrastructure growth. Over the past decade, high rises, new cities and modern road networks have become an increasingly common sight not just in the commercial capital of Colombo, but throughout the country. For a country that always mainly relied on roads which were built many decades back, the expressways connecting Colombo to the country’s southern province and the country’s main international airport have no doubt become two of the Sri Lanka’s most success stories in terms of the country’s expressway network.

The statistics itself is testament to the demand that Sri Lankans have for expressways, which makes the country’s only three expressways, the Southern Expressway, the outer-circular highway and the Katunayake Expressway, success stories in Sri Lanka’s developing road network.

The Southern Expressway (from Kottawa to Galle) was open to the public in 2011, followed by the Katunayake Expressway which connects Colombo directly to the Bandaranaike International Airport in Katunayake, which was open in 2013. The Southern Expressway subsequently was extended from Galle to Matara and this new stretch was open for public use in 2014, along with the Phase 1 of the Outer Circular Expressway, while the Phase II of the Outer Circular Expressway was subsequently completed in 2015.

The success stories of these vital expressways no doubt has warranted consecutive governments in power to seriously focus on expanding the road network in the country connecting the commercial capital to other key cities across the island, which will lead to enhanced efficiency, time saving which would also have a positive bearing on the country’s economic landscape.

Yet another vital expressway, the Colomb0-Kandy Highway and the Phase III of the Outer Circular Expressway as well as the Matara–Mattala extension which is part of the Southern Expressway will be declared open to the public in the near future. Refer Figure- I for a summary of expressway networks in Sri Lanka

Figure I: Expressway Networks and the Stage of Completion

Land Price Index of Sri Lanka (LPI)

The Central bank of Sri Lanka measures the land price movements in the Colombo District from 1998 onwards. The Land Price Index covered 5 divisional secretariats until 2017, when it was broadened to cover the entire Colombo District. Five divisional secretariats originally covered in the LPI were Colombo, Dehiwala, Homagama, Kesbewa and Kaduwela. Table I indicates the movements in LPI during the 2012-18 period.

Table I: Movements in Land Price Index of Sri Lanka

| LPI for Colombo District (Base period: 1998) | 2012 H1 | 2012 H2 | 2013 H1 | 2013 H2 | 2014 H1 | 2014 H2 | 2015 H1 | 2015 H2 | 2016 H1 | 2016 H2 |

| Residential LPI | 355 | 369 | 408 | 439 | 449 | 477 | 519 | 543 | 574 | 615 |

| Commercial LPI | 362 | 379 | 417 | 447 | 459 | 478 | 513 | 556 | 585 | 624 |

| Industrial LPI | 330 | 347 | 382 | 408 | 421 | 436 | 457 | 494 | 515 | 559 |

| Overall LPI | 349 | 365 | 402 | 431 | 443 | 464 | 496 | 531 | 558 | 599 |

Source: Central Bank of Sri Lanka

| LPI for Colombo District (Base period: 2017) | 2017 H1 | 2017 H2 | 2018 H1 | 2018 H2 | Y-o-Y change % (2018 H1) | Y-o-Y change % (2018 H2) |

| Residential LPI | 100 | 107 | 116.5 | 125.4 | 16.50% | 17.20% |

| Commercial LPI | 100 | 107.3 | 116.8 | 125.9 | 16.80% | 17.40% |

| Industrial LPI | 100 | 106 | 115.8 | 126.6 | 15.80% | 19.40% |

| Overall LPI | 100 | 106.7 | 116.3 | 125.9 | 16.30% | 18.00% |

Source: Central Bank of Sri Lanka

Movements in Real Estate Prices along the Expressways

With the construction of expressways in the county, the land prices located specially near the exit points of the Southern and Outer Circular Expressways have skyrocketed during the period between 2012-15. The easy access from Colombo to the Southern Province also resulted in an increase in apartment complexes, office buildings specially in and around the Galle district, which up until recently was unaccustomed to such forms of developments which also includes high-rise buildings. Table II indicates the land price movements near the exit points of the expressways.

Table II: Land Price Movements along the Southern and Outer Circular expressway

| Access point | City | Land Price in 2012 | Land Price in 2015 | % increase | 3 year CAGR % |

| Kottawa | Kottawa | 235,000 | 425,000 | 81% | 22% |

| Pannipitiya | 210,000 | 447,500 | 113% | 29% | |

| Gelanigama | Panadura | 90,000 | 202,000 | 124% | 31% |

| Dodangoda | Kalutara | 47,000 | 69,000 | 47% | 14% |

| Welipenna | Aluthgama | 55,000 | 82,000 | 49% | 14% |

| Kurundugahahethkma | Ambalangoda | 42,000 | 75,000 | 79% | 21% |

| Athurugiriya | Athurugiriya | 220,000 | 290,000 | 32% | 10% |

| Hokandara | 210,000 | 312,000 | 49% | 14% | |

| Kaduwela | Kaduwela | 130,000 | 190,000 | 46% | 13% |

| Malabe | 320,000 | 470,000 | 47% | 14% | |

| Kadawatha | Kadawatha | 190,000 | 255,000 | 34% | 10% |

| Weliweriya | 56,000 | 136,250 | 143% | 34% |

Source: Public information

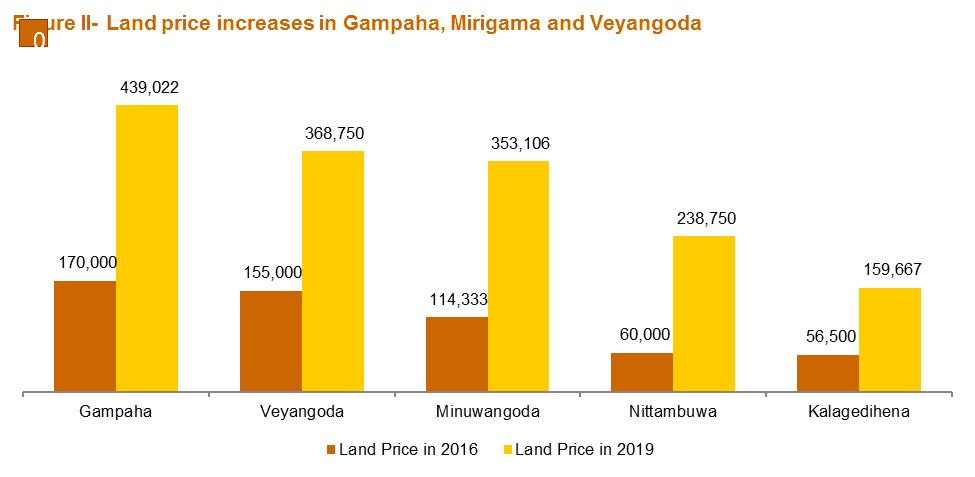

With construction work for Colombo Kandy Expressway kicking off in 2015, there has also been an increase in the land prices in the adjacent areas where the expressway is currently being constructed. For example, we noted a significant increase in the land prices around Gampaha, Mirigama and Veyangoda during the 2016-19 period as illustrated in Figure II and table III.

Source: Public information

Table III: Land price increases in Gampaha, Mirigama and Veyangoda

| City | Land Price in 2016 | Land Price in 2019 | % increase | 3 year CAGR % |

| Gampaha | 170,000 | 440,000 | 159% | 37% |

| Veyangoda | 155,000 | 370,000 | 139% | 34% |

| Minuwangoda | 115,000 | 355,000 | 209% | 46% |

| Nittambuwa | 60,000 | 240,000 | 300% | 59% |

| Kalagedihena | 56,500 | 160,000 | 183% | 41% |

Source: Public information

With the construction of the expressways, many property development companies have launched both land development and apartment projects along the expressways, capitalizing the ease of commuting to and from Colombo.

How should we read this information as investors in real estate?

While the land prices may depend on the locality and unique factors relating to the specific property being considered, we may need to pay attention to the general trends in land prices along the expressways to time the investments. Therefore, it is increasingly important to understand the potential upside already captured in the current price, in anticipation of the future completion of the expressways. If we are employing the same analysis for the Colombo-Kandy expressway, we may look at cities given in table IV close to the exit points.

Table IV: Cities along the Colombo- Kandy Expressway

| Exit Point | City |

| Nakalagamuwa | Dambadeniya |

| Narammala | |

| Polghawela | |

| Pothuhera | Pothuhera |

| Dambokka | Dambokka |

| Kurunegala | |

| Boyagane | |

| Galadedara | Galagedara |

| Mawathagama | |

| Katugastota | |

| Poojapitiya |

Another potential for the investors is to identify the arbitrage opportunities provided by the Colombo – Port City elevated highway and the New Kelani Bridge- Athurugiriya expressway. When the Colombo Port City is completed, it is believed that part of its work force will not be living inside the Port City. Such people may seek affordable accommodation in the vicinity of the Port city. As of now the land prices in Colombo 1, 3 and 7 are in the range of 15 to 17.5 million per perch. However, the elevated highways may provide easy commute between other cheaper cities within or close to Colombo Municipality and Port city. Please refer table V for such cities.

Table V: Cities close to Port City

| Access Point | City | Distance from access Point | Land Price (per perch) |

| Grandpass | Grandpass | 0.0 km | 4,350,000 |

| Orugodawatta | Wellampitiya | 1.9 km | 970,000 |

| Sedawatta | 1.2 km | 900,000 | |

| Dematagoda | Dematagoda | 0.0 km | 4,600,000 |

| Kolonnawa | 1.8 km | 900,000 | |

| Borella | 1.8 km | 8,000,000 |

Source: Public information

The nexus between property development and expressways

Property developers no doubt can take advantage of the various new expressways in the pipeline by planning ahead and investing in areas which are in close proximity to these expressways and exit points, which no doubt will see an increase to the price point in the coming years.

(- PricewaterhouseCoopers (PwC) Sri Lanka is an independent entity which is a part of the PwC global network. PwC Sri Lanka employs more than 500 people including 19 Partners and Directors who are dedicated to solving complex problems that businesses are facing in today's changing marketplace. -)