Aug 18, 2020 (LBO) – Aspiring digital bank entrants in Asia may struggle to attain the critical mass necessary to reach business viability amid the pandemic-related economic shock, especially in developed markets where competition from incumbent banks was already fierce, says Fitch Ratings.

Nevertheless, digital banks in the Asia-Pacific (APAC) with the right pedigree and financial and technological resources should still be able to realise the region’s market potential in the longer term.

Social-distancing and lockdowns associated with the pandemic have accelerated the shift towards digital services, including banking. However, the flight to quality during the crisis has also benefitted established banks, in terms of access to funding. The crisis has also forced established banks to accelerate their digitalisation efforts, reducing the risk of complacency and potentially closing off openings for new entrants.

buy antabuse online http://annalsofhealthresearch.com/classes/core/php/antabuse.html no prescription

Meanwhile, the primary target segment for many virtual banks in APAC – the unbanked and underserved – has been disproportionately hit by the economic shock, reducing opportunities for profitable lending. At least in the near term, we believe these adverse effects will more than offset the impact of greater digital usage.

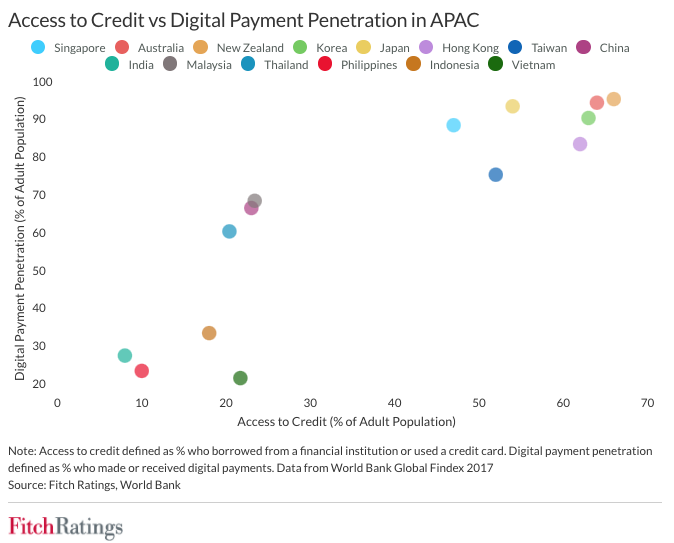

Fitch continues to believe that the greatest opportunities for virtual banks to tap underserved potential customers in APAC lie in emerging markets like India, Indonesia and the Philippines, where banking service penetration remains low. This gives them an easier path to critical mass.

However, these countries are among the worst affected by the pandemic in the region, and even in the longer term, their potential may be hampered by lagging digital infrastructure. Moreover, there remains a risk that aspiring virtual lenders may misprice credit risks when targeting the unbanked, notwithstanding their potentially more advanced data analytics capabilities.

Although some digital banks in APAC have already turned profitable, such as Tencent-backed WeBank in China and the eponymous KakaoBank in Korea, most digital-only lenders’ risk frameworks and business models have not been tested through the economic cycle. The current particularly steep downturn could reveal weaknesses in the approaches of some virtual banks. In Europe, for example, the uncertainties created by the pandemic have exacerbated the challenges UK-based online bank Monzo faces regarding the viability of its business model.

The challenges presented by the pandemic have reinforced our belief that there is likely to be limited rating impact on our portfolio of banks from the entrance of virtual banks in the near term. However, those digital banks that are able to survive or thrive through the downturn are likely to be better-resourced and may pose a greater competitive threat over the medium term to digitally unprepared rivals.

We would view smaller banks in jurisdictions with weaker digital banking capabilities as being more vulnerable to such disruption. In markets with dominant incumbents like Australia, Hong Kong, Japan and Singapore, aspiring neobanks may face difficulty out-investing leading conventional banks in digitalisation to offer a distinctive value proposition beyond niche areas.

The virtual banks likely to provide more formidable competition for incumbents over the medium term include those backed by established technology platforms, such as Facebook or Alibaba, or deep-pocketed corporates, such as Reliance or Singtel, These backers are more likely to be able to sustain the heavy financial investment necessary for entrants to attain scale, maintain cost competitiveness and survive the initial loss-making stages of a start-up. Strong name recognition associated with the parent may also help to generate credibility and aid in building a customer base, as well as providing potential synergies that may give the lending business a competitive edge.