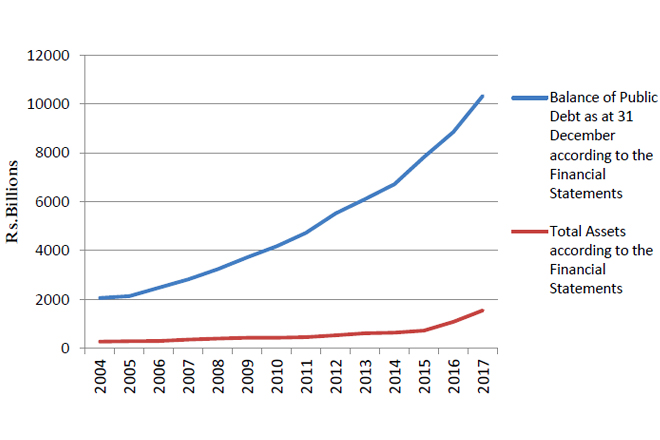

Feb 09, 2018 (LBO) – Auditor General's Department says even if the total amount of domestic and foreign debt payable by the government as at 31 December 2016 stood at 8.9 trillion rupees, in financial statements, the value of the total assets only shows 1.1 trillion rupees.

Their latest report on the public debt management has identified that the failure to utilize the total net borrowings sufficiently in keeping with the estimations in the investments activities and failure to correctly identify and account the assets derived from there had been the immediate reason for this.

The objective of this report was to forward an analytical report on the management of debt during the period from 01 January 2005 to 31 December 2016 to Parliament.

“Even though the financial statements had been termed as financial statements of the republic, those had been confined solely to the transactions of the consolidated fund,” AG Department said.

“Accordingly, transactions and events of the Provincial Councils, Local Government Authorities, Public Enterprises and other institutions owned by the republic or functioning under the government had not been incorporated in these financial statements.”

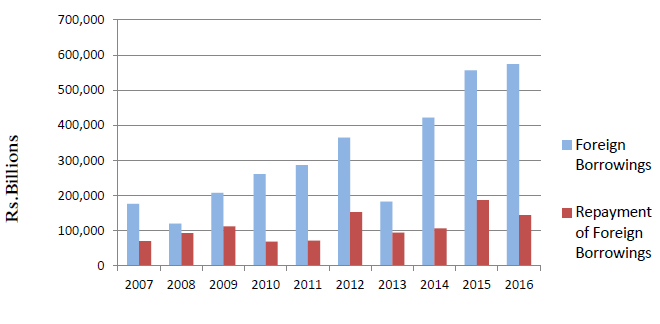

AG Department said a significant amount of total net borrowings obtained by the government had been utilized for the daily needs including expenditure of recurrent nature.

The report highlighted that the existence of the balance of debts not included in the financial statements and the existence of foreign debt not accounted due to lack of provisions although realized.

Meanwhile, releasing a statement contrary to this, the Central Bank said central government debt compiled by them has been reviewed and accepted by international agencies including the IMF.

“CBSL wishes to emphasize that to-date, the Government of Sri Lanka has maintained an unblemished record of debt servicing made in accordance with service payment obligations recognized through debt recording systems,” CB said.

“Further, towards prudent management of Government debt portfolio, a debt management strategy is being formulated by CBSL for implementation and it is also in the process of streamlining debt servicing liabilities with the passage of Active Liability Management Act.”

Executive Summary of AG's Public Debt Management report on Feb 2018

Necessity for the preparation of a special report regarding Public Debts Management in Sri Lanka was observed according to the matters revealed during the course of audit test check conducted on the financial statements of the Democratic Socialist Republic of Sri Lanka pertaining to the year ended 31 December 2016. Accordingly, this report is issued in addition to the report presented by me in respect of the aforesaid financial statements in pursuance of the provisions in the Article 154 (1) of the Constitution. The objective of this report is to forward an analytical report on the management of debt of the Republic of Sri Lanka during the period from 01 January 2005 to 31 December 2016 to Parliament.

(i) Even though the above financial statements had been termed as financial statements of the Republic, those had been confined solely to the transactions of the Consolidated Fund.

buy levaquin online

buy levaquin online no prescription

Accordingly, transactions and events of the Provincial Councils, Local Government Authorities, Public Enterprises and other institutions owned by the Republic or functioning under the Government had not been incorporated in these financial statements.

(ii) According to the financial statements furnished to Audit, the total amount of domestic and foreign debt payable by the Government as at 31 December 2016 approximately stood at Rs.8.9 trillion (Rs.8,860,770 million). Nevertheless, according to the financial statements, the value of the total assets accounted was approximately Rs.1.1 trillion (Rs.1,087,225). Failure to utilize the total net borrowings sufficiently in keeping with the estimations in the investments activities and failure to correctly identify and account the assets derived therefrom had been the immediate reason for this purpose.

(iii) Even though the burden of debts of the country was rapidly on the increase, the non financial assets had not increased relatively.

(iv) A significant amount of total net borrowings obtained by the Government had been utilized for the daily needs. (Expenditure of recurrent nature)

(v) Continuous increase in the per capita debt.

(vi) Decrease in the actual financing (to meet the budget deficit) as compared with the revised Budget and correspondingly, decrease in the anticipated total borrowings in the year 2016.

(vi) Existence of the balance of debts not included in the financial statements.

(viii) Existence of foreign debt not accounted due to lack of provisions although realized.

It was observed according to the above matters that the management of public debt remained at extremely poor position and the control of increase in the public debt balance can be identified as an indispensable matter. Similarly, the public debt obtained should be efficiently, economically and effectively utilized and the management should responsible for the preparation, implementation and maintenance in an updated manner the suitable internal control mechanism to ensure that the debts are utilized in the above manner.

Further, it is an essential matter to use the all the public and non-public debt received by the country under the approval of a centralized institution and to introduce a methodology capable of identifying the balance of public debt at any time.