Opinion: The Capital Market Cure

By the Prince of Kandy:

The Monetary Board in conjunction with the Central Bank is busy creating a policy to create systems whereby there is a better transmission of monetary policy. The situation has become quite dire as the Central Bank seems to have lost control over interest rates. This is most evident in the Central Bank imposing regulation limiting the rate at which new deposits can be renewed[1].

The law states;

The maximum interest that may be offered or paid by a licensed bank on Sri Lanka Rupee deposits shall be based on the standing deposit facility (SDFR) or the Weighted Average Yield Rate (WAYR) of 364-days Treasury Bills (T-bill rate) This cap though has not yet resulted in a lowering of lending

rates. Banks have used the benefit of the intervention reducing the interest

paid to the saver and kept lending rates higher than the benefit accrued. In

other words, net interest margins have widened.

To quote the recent monetary policy statement[2];

However, all market lending rates, including the AWPR, are yet to show a downward adjustment commensurate to the decline observed in deposit interest rates. The Average Weighted New Deposit Rate (AWNDR) declined by 266

bps from end April to 8.58% in July 2019 and the Average Weighted New Fixed

Deposit Rate (AWNFDR)declined by 269 bps from end April to 8.88% in July 2019.

This is as Average Weighted Lending Rate declined by 25 bps

to 14.22% in July 2019 from end April and Average Weighted New Lending Rate

declined by 74 bps to 13.88% in July 2019 from end April. Average Weighted

Prime Lending Rate (AWPLR) declined by 147 bps to 10.77% as at 16th August

compared to 12.24% recorded at end April 2019.

The figures quoted for average weighted rates behave in the

manner a moving average would. The figures quoted for new deposits or lending

would only have an impact in proportion to their weight in the existing stock.

These averages are what the Central Bank has strongly

signaled that it is trying to improve.

It, however, isn’t fair in this context to label bankers as

being profiteers. Banks have an existing liability stock, i.e. fixed deposits

made in 2018 and earlier, and this holds steady their cost of funds.

The Average Weighted Deposit Rate (AWDR)for Aug 2019 (based

on July data) declined by 24 bps from end April to 8.73%. Average Weighted

Fixed Deposit Rate (AWFDR)for Aug 2019 (based on July data) declined by 41 bps

from end April to 10.74%.

Banks in Sri

Lanka only offer instruments with fixed

rates of return. Old deposits will still have to pay the rate of return

negotiated earlier until such time that they are up for renewal. This means

that even if all competitors are by regulation limited from offering high rates

it will take time for that to impact their cost of deposits.

Banks have also in the recent past been on the receiving end

of multiple tax increases. In the opinion of many, this is because banks tend

to be highly compliant with the law and as such prove an easy target.

This regulation on net interest margins and thereby

profitability comes as the banks have to raise considerable amounts of capital

to be BASEL

compliant. The Central Bank has set time spans and intermediate capital

requirements for BASEL

compliance.

Savers will probably end up diverting funds to risky

commercial paper made available through a weak and expensive offering of unit

trusts. Their rates are not regulated. This will reduce the growth of deposits

with the formal banking system.

Given better capital markets savers would opt for corporate

debt. However, the CSE and the SEC seem determined to prevent any such option

from developing.

If total credit does not grow sufficiently

and existing lending obligations are not repriced, then average weighted

lending rates would not decline to the 200 bps target. This would happen even

if the banks lend at rates agreeable to the regulator.

Here there is the opportunity to game the metric. Banks and

the regulator can collude by charging high fees on the repricing of

obligations. At the same time, they could bring down the interest rate.

To quote the recent monetary policy statement;

Private sector credit in absolute terms, declined marginally by Rs. 1.2 billion in July 2019. This is after a significant increase of Rs. 63.2 billion in June 2019 The cumulative increase during the first seven months of 2019 is Rs. 42.5 billion. Year on year growth of credit further moderated to 7.7% in July 2019 in comparison to 8.7% in June 2019. This is the lowest growth rate witnessed since December 2014. Both the governor and director

for economic research, Dr. Y M Indraratna called for concern with the reduction

in private credit growth.

Banks are now shy of raising

capital. Capital market conditions are depressed[3].

The two major development banks NDB[4]

and DFCC[5]

both failed to raise capital this year. This was even as they were offered at

significant discounts.

Regulatory uncertainty is

being driven by the shotgun merger rhetoric[6] of

the central bank. The treasury is compounding this by targeting the sector for

increased taxation. This makes it difficult for firms to raise capital.

Without being able to increase

capital the rate at which the balance sheet of the banks can grow is limited. This

constrains banks from making new loans.

The federal reserve has

signaled and acted in a manner to extend historically low rates[7]. Sri Lanka has

unusually high rates. This makes it a highly opportune time for banks to

implement existing shelved plans. Namely securitization[8]

and international loans by the state banks[9].

International loans are self-explanatory.

As earlier mentioned the

situation is dire and therefore any fixes must be implemented quickly. The

situations must also be plausible given the PESTAL factors of the country.

Government debt is now under

better management with the active liability management act. This has resulted

in the continual declining of rates on government securities[10].

Further, the governor is actively using phrasing referencing inflation

targeting at monetary policy announcements. Inflation is below even the lower

bound of the 5 percent target.

The treasury has strongly

signaled its conscientiousness of public debt. Foreign denominated debt has

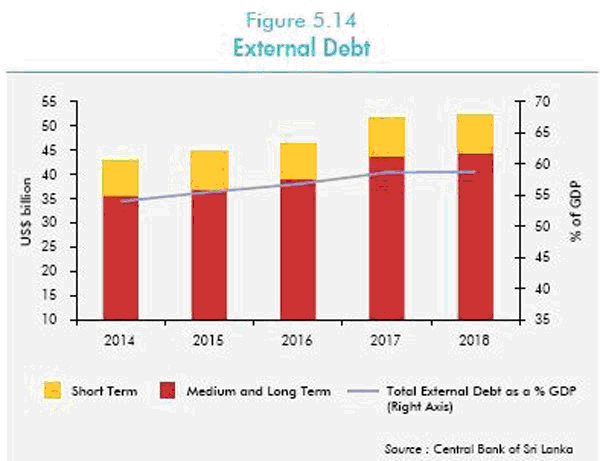

remained constant to GDP over the period. The external debt stock[11]

as at end 2018 was USD 52.3 billion which is 58.7 percent of GDP compared to

the previous year’s USD 51.6 billion which was 58.6 percent of GDP.

The objective of this strategy

would be to free up the balance sheets of the banking system to make new loans.

This would be a scenario wherein the banks and the regulator win. Further given

the tax structure it would be beneficial for banks to make more money from fees

than they do in the spread of lending and borrowing.

Securitization is the process

of parceling future revenue streams and selling them. Securitization became

more well known outside the world of finance following the 2008 global

financial collapse and the notoriety of mortgage-backed securities.

Given the nature of our

capital markets, securitization to third parties is not an immediate

possibility. However, most major banks own finance companies. Notably, Peoples

bank owns Peoples Leasing Company and Bank of Ceylon owns Merchant Bank of Sri Lanka.

These two institutions can

take on the loans of their subsidiaries to the extent that they optimize their

figures against the regulatory capital requirements. It would be wise to ignore

the internal political implications between top management and those subsidiary

companies. This is because if you had space to lend at lower margins the

Central Bank has signaled that it would force you to do so.

To quote Indian Finance

Minister Nirmala Sitharaman in her budget speech[12];

“Non-banking financial companies play an increasingly important role in India’s financial system” Though our Central Bank may not want to admit it, the NBFI

sector is the lifeline to the SMEs. This is where credit growth for the expansion

of GDP can be most effectively stimulated.

Politicized programs like Enterprise Sri Lanka which offer

interest rate subsidy through considerable bureaucracy do not work in the long

run. Worse still are the bailout programs to predatory microfinance companies[13]. It

would be far more effective if the treasury acted to free up the balance sheet

of lenders on the basis of a track record of promoting enterprise.

The banking system is reflective of power in society. To whom

loans are disbursed and at what rate are for the most part decided within those

institutions. These assessments can have self-fulfilling impacts on

creditworthiness. In certain instances, it is easier for some people to get

lifestyle loans that they are unlikely to pay back than it is for businesses

with strong track records to borrow to expand.

That is because banks may collateralize a Colombo

home and not so one in Kandy.

This invariably has an impact on liquidity for the Colombo

residential market over Kandy.

Bob Hope said;

A bank is a place that will lend you money if you can prove that you don’t need it. Prime borrowers are the people who

get the Average Weighted Prime Lending Rate. This rate has dropped the most

according to the monetary policy data. This is because these borrowers have

bargaining power with the banks.

Banks, if forced to lend on a

short term time horizon, will probably do so by helping big companies refinance

their negative cash flow positions. This would also help reduce their immediate

default risk allowing management to postpone any difficult questions. Some

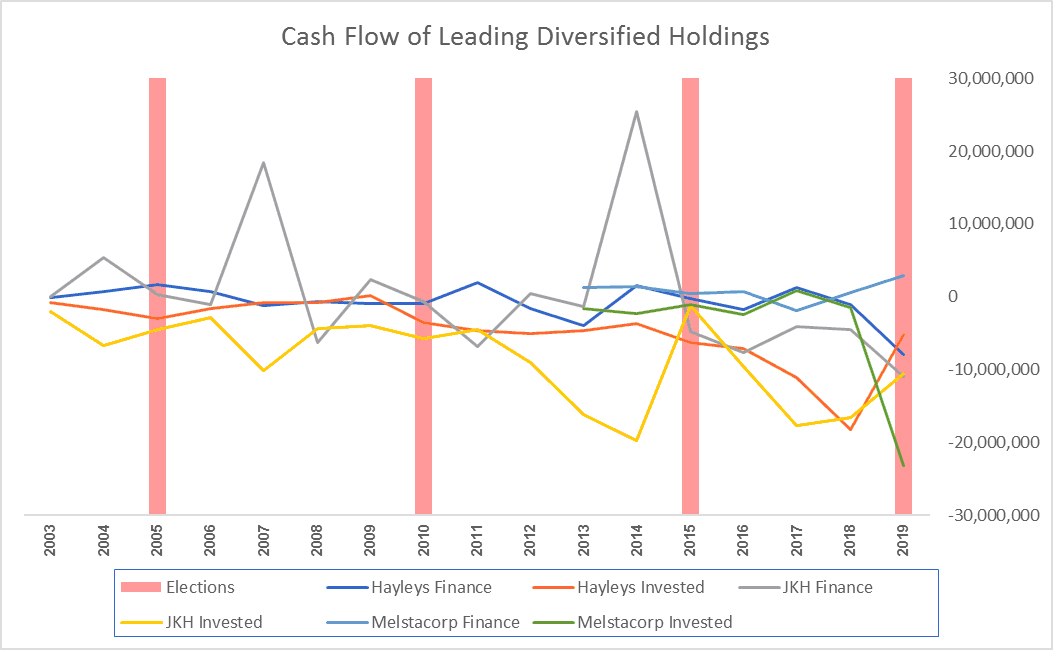

large corporates have quite sizable negative cash positions.

Given above are the cash flows of the three leading

diversified holdings groups in the country. No one invests during election

season. Note that Melstacorp’s investment figure for 2019 is linked to its

takeover bid on John Keells and not really linked to new investment in the

economy.

Big companies are in a position to plan their investments in

line with government policy. They, therefore, wait to see who the government is

going to be and what they plan to do. They do not want to be in a position

where their investments go against government policy.

One may recall that supermarkets were targeted under the

Rajapaksa government in order to help small retailers. One would also note that

it was the sweetened beverage and food industry that was first to meet with the

purported coup government[14].

It is currently very difficult to see what will happen

politically. I myself did not think that Mahinda would select Gothabaya

Rajapaksa and still feel something does not add. In such a context it is

unlikely to see any large scale investment in the near future.

If the Central Bank is serious about the output gap it should

consider helping the Non-Bank Financial institutions. They are the institutions

capable of creating a boom in the SME sector. [1]https://www.cbsl.gov.lk/sites/default/files/cbslweb_documents/laws/cdg/bsd_circular_letter_20190628.pdf

[2] https://t.co/eK4DfZ5oCC?amp=1

[3] http://www.dailynews.lk/2019/03/11/business/179837/aspi-falls-lowest-sept-2013

[4] https://cdn.cse.lk/cmt/uploadAnnounceFiles/7451545389632_386.pdf

[5] https://cdn.cse.lk/cmt/announcement_portal_prod/dfcc_3589040472812898.pdf

[6] http://www.sundaytimes.lk/190526/business-times/cb-gets-tough-with-licensed-finance-companies-350366.html

[7] https://www.theguardian.com/business/2019/jul/31/federal-reserve-cuts-interest-rates-by-025-its-first-in-a-decade

[8] http://www.sundaytimes.lk/180325/business-times/securitisation-bill-to-be-ready-by-next-year-287105.html

[9] https://www.businesstimes.com.sg/banking-finance/sri-lanka-state-banks-to-borrow-up-to-us1b-abroad-before-end-of-2018

[10] https://economynext.com/Sri_Lanka_s_Treasury_Bill_yields_continue_fall_across_maturities-3-15171.html

[11] http://www.dailynews.lk/2019/05/22/finance/186196/%E2%80%98marginal-increase-external-debt-stock%E2%80%99

[12] https://www.financialexpress.com/budget/budget-2019-why-nirmala-sithraman-says-nbfcs-need-parity-with-banks-on-tax-issues/1631755/

Like Moving Averages

Are Banks Profiteering?

Banks as Victims

Private Credit Growth Has Contracted

Capital Limitations

The Capital Market Fix

Context

Objective

Securitization

In a Local Context

Why Finance Companies?

How Banks would Lend otherwise

This would not Result in investment