Nov 23, 2020 (LBO) – Moody’s Investors Service does not expect Sri Lanka's 2021 budget to provide a meaningful boost to output, while increased spending will also add to fiscal pressures, a credit negative.

"We expect the government to face challenges in rationalizing government spending and delivering fiscal consolidation postcoronavirus, as a large interest bill, rigid public sector wages, and subsidies and transfers keep recurring government spending elevated," Moody’s Investors Service said.

"The dilemma between delivering on ambitious fiscal consolidation targets and supporting economic recovery will continue to weigh on Sri Lanka's credit profile ahead of significant and recurring external debt-servicing requirements through 2025."

Moody’s Investors Service expect Sri Lanka’s economy to contract by more than 3% in 2020, with prospects for a gradual rebound in 2021 increasingly at risk given renewed virus flare-ups and lockdown measures globally.

Full Statement

On 17 November, Sri Lanka's (Caa1 stable) Prime Minister and Minister of Finance Mahinda Rajapaksa presented the proposed 2021 budget. The budget calls for LKR3.6 trillion ($19.5 billion, 23.7% of 2020 forecast GDP) in expenditure, a 26% increase from its estimate for 2020. Despite the growth focus of the budget, we do not expect it to provide a meaningful boost to output, while increased spending will add to fiscal pressures, a credit negative.

The budget targets a 2021 fiscal deficit of 8.8% of GDP, compared with a revised 2020 estimate of 7.9% of GDP. We forecast a similar gap for 2021, but for the deficit to remain above 8% of GDP through 2023 in light of persistently adverse fiscal dynamics and a slow economic recovery. As such, we expect Sri Lanka's debt burden to increase to around 100% of GDP over 2020-21, above the Caa-rated median of 88% of GDP, and only begin to gradually decline in subsequent years.

We expect the government to face challenges in rationalizing government spending and delivering fiscal consolidation postcoronavirus, as a large interest bill, rigid public sector wages, and subsidies and transfers keep recurring government spending elevated.

The dilemma between delivering on ambitious fiscal consolidation targets and supporting economic recovery will continue to weigh on Sri Lanka's credit profile ahead of significant and recurring external debt-servicing requirements through 2025.

Economic boost from budget will be limited. The budget includes large allocations for domestically financed infrastructure development, incentives for domestic production, support for small and medium-sized enterprises and upgrading Sri Lanka's rural road networks, to which the largest portion of public investment spending has been allocated. It also includes scaled-up support to the tourism industry, which has taken a severe hit given the country's border closures.

But despite the focus of the development-oriented budget on reviving economic growth and reducing poverty, the benefits will be limited by the magnitude of the pandemic-driven hit to demand for Sri Lankan exports and the collapse in tourism activity. Domestic demand is also likely to remain sluggish given still-subdued business and consumer confidence, and ongoing import restrictions affecting industries such as construction and manufacturing.

We expect Sri Lanka's economy to contract by more than 3% in 2020, with prospects for a gradual rebound in 2021 increasingly at risk given renewed virus flare-ups and lockdown measures globally.

The plan to support domestically financed infrastructure projects may also face funding constraints as a weak economic recovery curbs revenue and as rigid recurrent expenditure is difficult to rationalize. The budgetary allocation for public investment has increased to LKR1.1 billion, up more than 55% from government estimates for 2020 spending.

buy lexapro online buy lexapro online no prescription

Even as the government begins to digitalize government systems and processes, including procurement, and implement reform of state-owned enterprises, these reforms will not meaningfully consolidate public expenditure.

On the revenue side, the budgeted 28% increase in government revenue compared to 2020, largely stemming from robust growth in taxes on goods and services, and external trade, is unlikely to be achieved. A recovery in demand for Sri Lankan exports in 2021 is increasingly at risk given the uneven economic trajectory in major markets like the US (Aaa stable) and Europe.

While the budget introduces some modest revenue-enhancing measures, including simplification of capital gains taxes and implementation of an e-filing system, we do not expect stronger economic growth alone to rebuild Sri Lanka's revenue base, from an already narrow position.

Revenue-to-GDP has steadily declined from 14.1% of GDP in 2016 to an estimated 9.5% of GDP in 2020, an outcome of a multi-year period of sluggish economic growth, weak tax administration implementation, and rate changes, including the December 2019 valueadded tax cuts,1 which the government has committed to maintaining over the next five years.

Fiscal consolidation challenges could hinder finance raising needs. Alongside the 2021 budget, the government presented its medium-term macro fiscal framework, which targets a reduction in the fiscal deficit to 4% of GDP, to bring down the government's debt-to-GDP ratio to 75.5% by 2025. This goal is supported by medium-term goals of real GDP growth at 6% or above per annum and revenue-to-GDP over 14%.

The risks clouding the near-term economic recovery and obstacles around fiscal consolidation are likely to pose hurdles to achieving these ambitious targets, especially putting the government's debt-to-GDP ratio on a more sustainable, downward path.

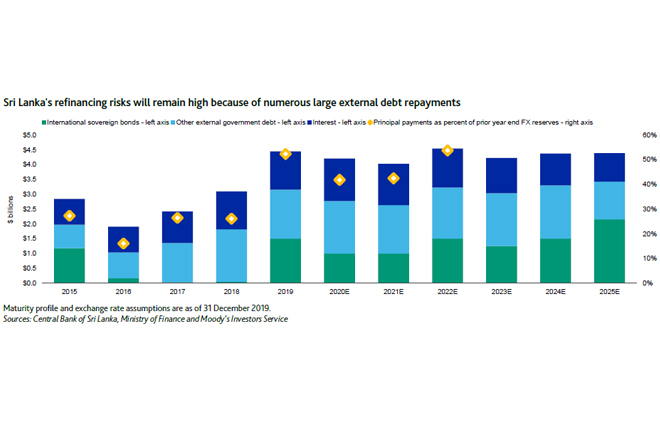

A bleaker outlook for fiscal consolidation is likely to continue to challenge the government's ability to raise financing for upcoming debt obligations and narrow annual borrowing needs, which in 2021, externally, amount to approximately $4 billion. Borrowing needs will stay elevated through 2025, including a large portion of maturing international sovereign bonds (see exhibit). Elevated repayment risks will continue to raise pressure on the government's external and liquidity position as the recovery in major sources of foreign exchange earnings is likely to be slow, keeping the country's international reserves position thin.