Following a year of volatility, leading stockbroking firm Asia Securities (Pvt) Ltd, notes that the road ahead for Sri Lanka’s capital markets is optimistic, with the ASPI expected to reach 7,400-7,600 in 2021.

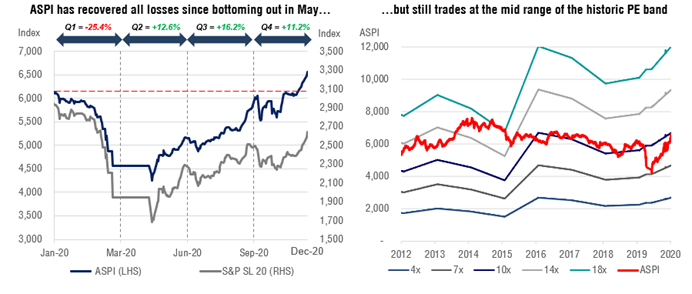

The Sri Lankan stock market marked a V-shaped recovery in 2020, seeing one of its strongest rallies to recover all losses suffered over the course of the coronavirus pandemic.

The latest Asia Securities Sri Lanka: 2021 Equity Outlook report titled ‘Zero in on the Recovery’ highlights that the forces behind one of the fastest recoveries include a low interest rate environment, manufacturing-dominance led by protection for local firms, and renewed economic hopes and policy stability with both the Presidential and Parliamentary elections now behind.

A strong bounce back from historic lows

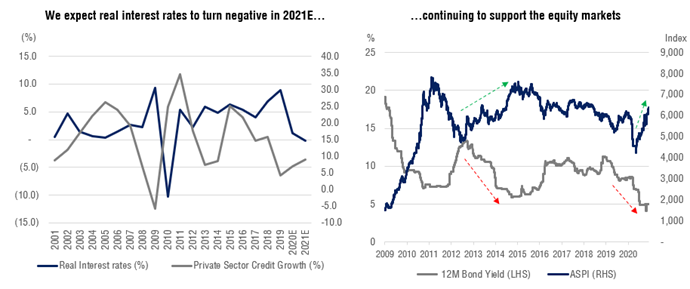

The report highlights that “Low interest rates locally continue to provide further impetus for the market to rally and local investors will continue to carry the mantle in 2021. Despite the likelihood of rates bottoming out once credit growth picks up, we expect equities to remain the more attractive asset class as rates will be recovering from a historic low.”

Further upside to ASPI amidst historically low interest rates

In addition to low interest rates, the strong trajectory for Sri Lanka equities is supported by an improvement in earnings (coming from a lower base), and large caps gaining momentum with earnings picking up. The Asia Securities report also forecasts a healthy pickup in corporate earnings in 2021 driven by consumption-related stimuli, and lower finance costs which will help the bottom line.

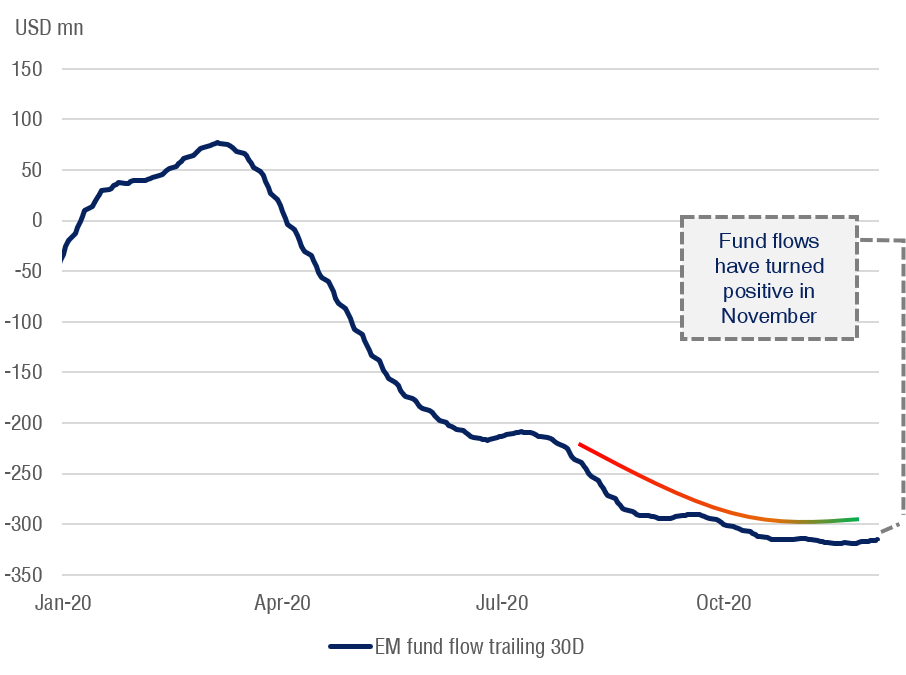

Emerging markets ready for primetime in 2021, however, Sri Lanka to see latent fund flows

Asia Securities Research said that the momentum in equities from this point forth will also be dependent on how certain global factors playout. Emerging markets are expected to take off again in 2021, breaking a decade-long trend of asset allocations towards developed markets amidst superior growth, a strengthening USD, and strong yields. Several factors will drive this shift, including:

- Weaker USD in the medium-term – A weakening USD will push investors to rebalance their portfolios and spur capital flows into emerging markets. With lower currency risk, Asia Securities Research sees cheaper emerging market valuations being more appealing and rewarding for investors.

Emerging markets set for a 2021 takeoff

- Faster growth than developed markets – Bloomberg consensus point at emerging markets growing (real GDP) at a faster 5.0% in 2021E, compared to 4.0% for developed markets. (2022E; emerging markets – 5.1%, developed markets – 3.1%). One of the main reasons for a faster emerging markets recovery is better management of the pandemic. With stronger growth prospects and low currency risks, Asia Securities Research notes that emerging markets are in a “sweet spot” in 2021.

- Lower valuations – While emerging markets have underperformed the S&P 500 over the last decade, earnings expectations have been on the rise with hopes of a faster recovery.

- Low interest rates – As it is still a struggle to find yield in government bonds amidst low interest rates, a risk-on approach with global recovery will drive funds to faster growing emerging market economies.

- Trade – The election of Joe Biden represents a return to more predictable US politics. An easing of trade tensions between US and China can further aid recovery in the Asian Markets.

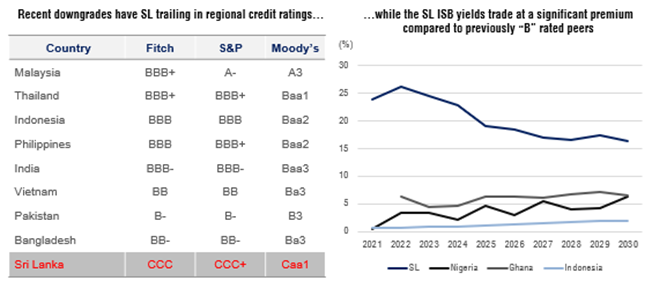

While a risk-on sentiment with vaccine deployment and global recovery will favour equities in 2021, Asia Securities Research highlighted that regional countries are likely attract foreign fund flows first, with Sri Lanka seeing latent fund flows. Concerns around Sri Lanka’s low credit rating mean that Sri Lankan equities can expect a very gradual improvement in foreign fund flows.

Asia Securities Research recommend rotation towards “COVID recovery” beneficiary stocks

Asia Securities’ key picks for 2021 are weighted towards consumer sector, as well as cyclical stocks that look attractive in a path to recovery. Corporate earnings will see a healthy pickup in 2021 driven by consumption-related stimuli, and lower finance costs which help the bottom line. In addition, free cash flow generation should remain strong, given that corporates will operate in an environment fueled by tax cuts early in late 2019/early 2020. Local manufacturing is also expected to see improved utilisation with higher protection. With an accommodative fiscal policy and consistent tax policies, the effects of the tax cuts (yet to materialize given the timing and impact of COVD-19) are also expected come to fruition in 2021.

| BANKS The valuation overhang is largely due to the uncertainty caused by COVID 19 on the already-stressed balance sheets of the banks. We expect credit demand to pick up in 2021, as the lockdowns gradually ease, and the prospect of a vaccine improving sentiment. In addition, the continued low rate environment and the corporate taxes, coupled with the focus on local manufacturing would lead to better growth, while sectors such as construction will gradually recover from the tight credit conditions. Along with this, the cost of risk should trend lower in 2021, and supported by maintained tax cuts, we expect earnings to mark a growth along with an improvement in ROE. | |

| INSURANCE We see low interest rates and insurance tax deductible allowance of LKR 1.2mn p.a, as strong incentives for life insurance demand to see robust growth going into 2021E. Life will also see a regulatory increase in the rate used to calculate Life contract liabilities, temporarily which will see to normalizing allocations to the life fund. With vehicle import restrictions looking to be extended to mid-2021, General insurance GWP will remain challenged. Investment yields to stabilise in CY21 before recovering in 2H. | |

| TELECOMMUNICATIONS Data usage has been strong, especially with the lockdowns inducing more sticky usage with e-commerce, e-learning and streaming media services. We believe this trend would continue in CY21E, backed by continued lower consumer taxes and higher disposable income. Higher network utilization, coupled with the roll-back of concessions offered during COVID-19 would support better profitability but will be offset to some extent by the falling away of the one-off cost savings seen in CY20 (e.g., marketing spend). We expect to see higher capex by both players as mobile network portability would come into effect and initial 5G capex would start. | |

| CONGLOMERATES Hit on multiple fronts since April 2019, we expect the sector to see a meaningful recovery only post 1H FY22E, given the sector-wide exposure to leisure. Conglomerates which derive a large part of its earnings from consumer and related businesses would be the key beneficiaries. In addition, with steps taken to open up the borders would likely help conglomerates to minimise operating losses in CY21, leading to a recovery in earnings. | |

| FMCGR The inflated trading multiples and lower ROEs compared to historical returns are a result of the sector losses/low profits seen throughout the past year. Going into CY21E, with no significant incentives by the government, we expect demand and spending to be driven by a gradual recovery in economic activity and income levels normalising. Counters exposed to food retailing will continue to benefit as consumers remain more focused on spending on food and essentials. | |

| CONSTRUCTION Following a hiatus of three years, the construction sector is set to take off in 2021 with several elements lining up to spark growth. The main trigger comes from low interest rates that will drive a residential sector thrust. On the supply side, we see a stable LKR to be a key positive for the construction sector that largely relies on imported raw materials. However, commodities such as Copper and Aluminium are strengthening on the back of a recovery in industrial activity. We expect the cement industry to see the first signs of a pickup. | |

| MANUFACTURING The overarching driver for this sector is the Government support towards local manufacturing. The Apparel sector has shown resilience through the pandemic and is set to grow strongly in 2021. With better management of the pandemic, Sri Lanka has become a preferred destination for US brands amidst vendor consolidation programs. Upcoming capacity expansions to accommodate this leads to our positive view on the sector. We are also positive on the export names which were levered to take advantage of pandemic-driven demand who will continue to benefit for most of 2021. | |

| ALCOHOLIC BEVERAGES The absence of an excise duty increase through the 2021 budget remains a key positive for stable demand going forward while the proposed Special Goods & Services Tax could lead to less volatile duty changes. This would also result in stabilising demand migration from the legal market to the illegal market. In addition, players in this segment would see margin benefit from local sourcing as well. | |

| HEALTHCARE Fear of exposure to potentially undetected COVID-19 patients will continue to impact OPD footfall. Hospitals with a strong position in elective surgeries, will continue to see sustainable occupancies. However, those dependent more on communicable diseases care occupancies, will continue to see low demand as regular hand washing, and masks have reduced the incidents of such diseases. However, should the Government include the private sector in its COVID-19 management practices, we expect the large hospital chains to benefit more than smaller players. | |

| LEISURE With the expectation of an ROE of -1.9% for FY22E, the Leisure Sector is trading at a significant premium to historic in anticipation of a tourism bounce back on news of allowing tourist entry from January 2021. However, hoteliers believe that a mandatory 2-week quarantine, restrictions on movement and mode of transport will hinder demand for short-holiday goers; key segment for listed larger properties. Maldives is seeing noteworthy recovery in arrivals benefiting from long-stays, although recovery is not uniform. Source dynamics have shifted to more towards Indian, Russian and Middle Eastern markets. | |

| ENERGY A key risk we see is in a strengthening of energy prices with vaccine deployment and normalization in 2021. We are positive on the Renewable Energy sector with government concessions towards the sector in the 2021 budget. | |

| NON-BANK FINANCIAL INSTITUTIONS While expect credit demand to pick up in 2021 helping loan demand, we expect lease demand to remain muted amidst import controls. This, combined with the core capital requirement of LKR 2.5bn by December 2021 will add pressure on the smaller cap NBFIs. While we perceive the consolidation push as a positive for the sector, we maintain our Neutral view on the sector based on 1) pressure on asset quality, 2) higher core capital requirement and 3) low vehicle lease demand. |