By Nilupulee Rathnayake

Having weathered a challenging period marked by a deep economic crisis, Sri Lanka is now demonstrating positive signs of an economic upturn. Still, amidst limited homefront policy alternatives against an unfavourable global backdrop, a critical question arises: how will Sri Lanka's external sector cope in the face of these challenges?

Notably, import controls, initially imposed in response to the dearth of foreign exchange liquidity in the domestic market, are being largely eased. The government is actively seeking to forge partnerships with regional giants, aiming to strengthen trade relations through Free Trade Agreements (FTAs). Nevertheless, in the broader global context, the rise of geopolitical rivalries, slow growth and contracting demand in key markets create multiple uncertainties for Sri Lanka's external sector recovery.

Global Economic Developments: A Complex Web of Uncertainties

Globally, there are promising signs of economic progress in the near term. Supply chain disruptions, which significantly impacted various industries, have largely returned to pre-pandemic levels. Energy and food prices, having peaked during conflict-induced periods, have substantially subsided, alleviating global inflationary pressures faster than anticipated.

However, the global economic landscape remains overshadowed by a complex web of uncertainties. Political dysfunction in key economies and ongoing geopolitical rivalries present challenges. The United States' imposition of bans on certain exports to Chinese firms exemplifies the extant geopolitical tensions. This growing inclination towards trade interventions through industrial policies, subsidies, and import restrictions, driven by national security and environmental considerations, has the potential to impact the trajectory of globalisation. These developments carry substantial implications for emerging and developing economies, particularly those deeply reliant on a globally integrated economy, foreign direct investment (FDI), and technology transfers. Economies contending with burgeoning sovereign debt overhangs in particular, are expected to face heightened vulnerabilities. Having defaulted in early 2022, Sri Lanka is among the countries particularly affected by these global economic shifts.

Sri Lanka's Vulnerable Export Sector

In 2022, Sri Lanka recorded its lowest merchandise trade deficit since 2011, primarily due to reduced imports and an uptick in exports. Merchandise exports expanded by 4.9% in 2022 compared to the previous year, while import expenditure decreased by 11.4% in 2022 relative to 2021. The decrease in import expenditure stems from a combination of import restrictions and foreign exchange liquidity constraints.

However, as import controls ease and the economy gradually improves, a marginal increase in import expenditure is observed from June 2023 onwards. While improving consumer welfare and food security, this move may negatively impact the trade deficit this year, especially as global demand for Sri Lanka’s primary exports, like tea and garments face a downturn – the former triggered by high production costs and the latter by contracting foreign demand.

Sri Lanka's key export markets for garments, particularly in the US and Europe, are experiencing low growth and weakened demand since the fourth quarter of 2022. Consequently, monthly earnings from garment exports in August 2023 indicates a 26% decline compared to August 2022. Notable decreases in the import of Ceylon tea by prominent Sri Lankan tea importers in 2022 relative to 2021, including Russia (by 9.6%), the UAE (by 2.5%), and Turkey (by 47%), also highlight the vulnerability of Sri Lanka's export sector to external shocks. The tea market's condition has seen a modest improvement in 2023, though it has not been entirely resolved.

The concentration of Sri Lanka's exports in terms of products and markets has long been a source of concern, rendering the economy exceedingly susceptible to sector-specific shocks.

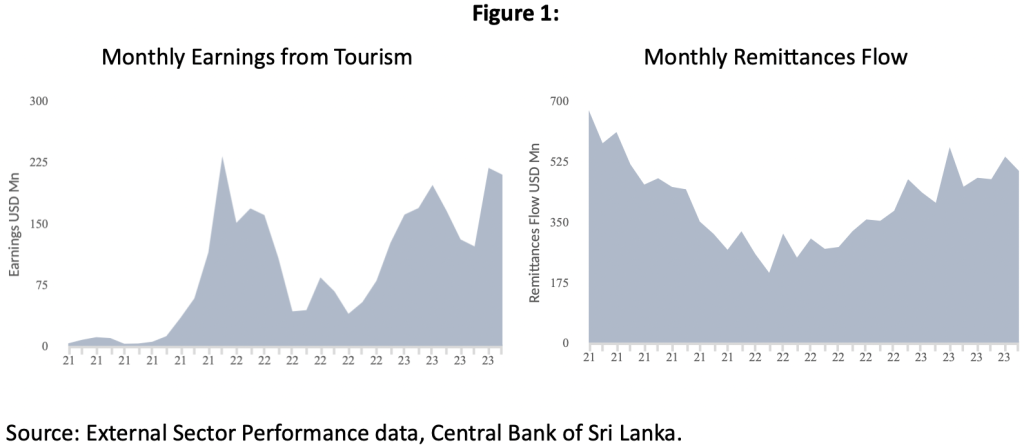

Tourism and Worker Remittances: A Silver Lining

In a positive trajectory, 2023 has witnessed a notable increase in monthly tourist arrivals compared to the previous year, signalling a discernible recovery trend. Cumulative tourist arrivals from January to August 2023 amounted to 904,318, compared to 496,430 arrivals recorded during the corresponding period in 2022. Overcoming the challenges within this sector necessitates a coordinated effort from various stakeholders, including the government and the private sector, as Sri Lanka endeavours to reconstruct its brand identity as a secure and preferred destination.

Worker remittances, representing another crucial source of foreign exchange earnings, have exhibited promise. In the first half of 2023, worker remittances grew to USD 2.8 billion, however it remains below the pre-pandemic level of USD 3.6 billion recorded in the first half of 2018. While the Middle East remains a vital destination for Sri Lankan workers, alternative destinations offering employment across various job categories have emerged, including South Korea, Singapore, Japan, and several European countries. Notably though, the large-scale migration of workers, including white-collar employees, raises concerns regarding long-term economic repercussions due to brain drain.

Challenges in Attracting Foreign Investment

In a fiercely competitive global FDI landscape, political stability and a robust macroeconomic framework are paramount considerations for investors, especially given the numerous countries competing for their attention.

In the post-war period, Sri Lanka experienced its peak FDI inflows in 2018, attracting USD 1.6 billion. However, in 2022, this figure dwindled to USD 898 million, reflecting the adverse impact of the pandemic and economic challenges. Sri Lanka's economic crisis – and the country's sovereign default status together with public protests, strikes, and violence – reshaped the country's perception as a not particularly attractive destination for foreign investors.

As Sri Lanka anticipates modest growth in the coming years, it becomes imperative not only to retain existing investors but also to proactively seek new investments within the current unfavourable climate. The Board of Investment (BOI) has targeted to attract USD 2 billion in FDI in 2023, with a particular focus on the tourism sector. An incentive package, potentially incorporating tax incentives, is being contemplated as a viable policy intervention, aligning with practices observed in peer countries aimed at attracting FDI.

Building Resilience and Diversification

Sri Lanka's external sector has been susceptible to policy missteps that exposed it heavily to external global shocks. Building the economy's resilience against external pressures must necessarily be a crucial part of the adjustment and recovery process. As import controls are also eased, to bridge the widening trade deficit, Sri Lanka needs to implement concrete policy measures to diversify its export basket and connect to global value chains.

Several initiatives have already been undertaken, for instance, to pursue fresh trade relationships with neighbouring giants. These trade agreements should be deep trade agreements that target not only merchandise trade but also services, FDI promotion, value addition, trade facilitation, and digitisation. In the near term, negotiations are ongoing on various stalled trade agreements with India, China, and Thailand, amongst others, while expressing interest in joining the RCEP trade bloc in the medium term.

However, notably, Sri Lanka can no longer approach efforts to expand and diversify exports in a piecemeal fashion and FTAs on their own will fail to deliver. High energy costs, labour shortages, and scaling back on infrastructure spending, amongst others, impact the operating environment for businesses. Sri Lanka's longstanding structural bottlenecks must be overcome by implementing the necessary reforms to raise productivity for sustained growth if the country is to regain lost confidence in its economic prospects.

*This blog is based on the comprehensive chapter on the external environment in IPS’ ‘Sri-Lanka: State of the Economy 2023’ report.

Nilupulee Rathnayake is a Research Officer working on Macro, Trade and Competitiveness research at IPS. She holds an MSc in Development Economics from the University of Nottingham, United Kingdom, and a BA in Economics from the University of Colombo, Sri Lanka. (Talk with Nilupulee - nilupulee@ips.lk)