”s

May 18, 2020 (LBO) – The G-20 debt suspension initiative is unlikely to ease the significant credit challenges that the coronavirus pandemic has amplified in some frontier market sovereigns, Moody’s Investors Service said in a report today.

QUOTES FROM MOODY’S SECTOR IN-DEPTH REPORT

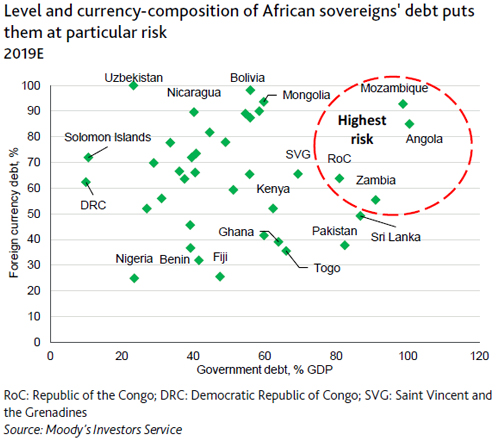

We rate 34 out of the 76 IDA-eligible countries, to which we add Bolivia, Sri Lanka and Vietnam that receive transitional IDA support as well as Angola.

We estimate that Angola, Vietnam, Pakistan (B3 RUR-), Bangladesh (Ba3 stable), Sri Lanka (B2 RUR-) and Kenya have the highest debt-service payments to official creditors as a share of GDP, at between 1% and 4%.

We expect that some countries such as the Maldives, Kenya, Mongolia, Pakistan, Sri Lanka will continue to register large fiscal deficits in 2021 and beyond.

By lowering debt-service payments at a time when government resources are limited and access to market financing is considerably constrained, the initiative will help to ease short-term liquidity pressures.

However, debt-service relief won’t have a significant impact on medium-term debt trends that have worsened during the crisis. Bilateral relief would only cover a fraction of the increased external funding gap resulting from the shock.

“While debt-service relief will allow some governments to reallocate scarce resources toward health and social spending, it will not have a significant impact on weaker medium-term debt trends,” said.

Lucie Villa, a Moody’s Vice President – Senior Credit Officer and the report’s co-author.

“The coronavirus shock will lead to sharply lower growth this year, wider budget deficits and higher debt burdens for at least the next few years, as well as higher borrowing costs, at least for debt contracted on commercial terms.”

“The prospect of significantly diminished revenue constraining debt-service capacity poses longerterm solvency challenges.”

The coronavirus shock and the authorities’ associated policy response have opened large fiscal and external imbalances that will take time to unwind. Low-income sovereigns entering the crisis with elevated debt burdens or exposure to foreign-currency risk are most vulnerable.

Moody’s estimates that the suspension of debt-service payments could reduce the funding needs of eligible Moody’s-rated sovereigns by about $10 billion over the next eight months. This would only cover a fraction of the external gap, leaving an outstanding shortage of around billion.

New official sector disbursements are expected to help fill the gap, including emergency financing from the IMF.