First Capital Research believes that there seems to be a high probability that Sri Lanka may consider moving into an IMF program.

Though there are rumours of negotiations, so far such a program has not materialized, but the Govt has obtained the Rapid Funding Facility of USD 787Mn from the IMF.

"Analysing the economic indicators and the forecast, we believe there seems to be an 85% probability that Sri Lanka may consider moving into an IMF program as soon as possible," First Capital Research said in its Mid-Year Outlook report.

Downgrades from Rating Agencies:

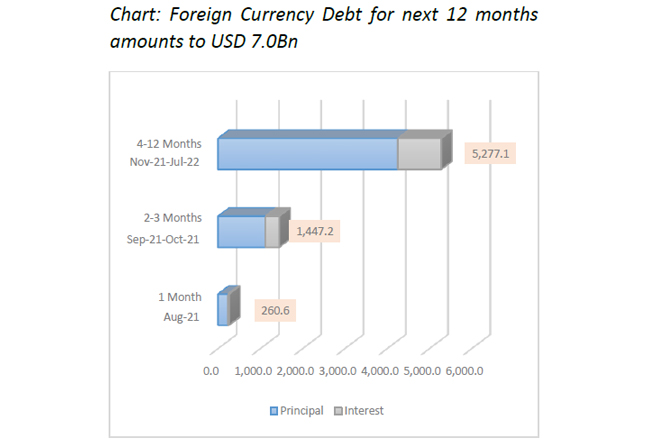

With the heavy debt burden and lower foreign reserves, two out of the three rating agencies have indicated potential downgrades. Foreign Currency debt repayment for the next 12 months amounts USD 7.0Bn compared to USD 2.8Bn of reserves as at Jul 2021.

"Though there is an improvement, the Balance of Payments is still in deficits, further deteriorating the foreign reserve position. We expect foreign reserves to fall to dangerously low levels of USD 3.5Bn by Dec 2021 and USD 3.0Bn by Jun 2022,"

Moody’s Rating for Sri Lanka currently stands at Caa1. The Outlook was recently changed to “Under Review”. Similarly, S&P Global has a rating of CCC+ for Sri Lanka and the agency recently downgraded the Outlook to Negative.

Fitch, however, has affirmed the rating for Sri Lanka at CCC. Fitch does not provide “Outlook” for countries with ratings of CCC and below.

As Sri Lanka is in the 2nd year of 10%+ budget deficit, potentially with an IMF program coming in there is a significant possibility for tax rates to be revised upwards, First Capital Research said.

Reduce equity exposure to 50%:

As the risk rises in the system supported by an increase in rates, First Capital Research recommends to further reduce the equity portfolio to 50% or aggressively shift the portfolio to defensive counters.

"Banking (mainly COMB, HNB, SAMP, NDB), selected dollar income companies (HAYC, TJL, WIND & LVEF – others have surged in price and cannot be highlighted as defensive anymore, Eg: EXPO, HAYL, MGT), dividend yielding counters (CTC, NEST, LLUB) and Life Insurance companies are the preferred defensive counters."