May 05, 2016 (LBO) – With slower growth in the next few years and signs of financial stress for some state-owned enterprises, achieving significant fiscal consolidation will be challenging, Moody’s said in a statement.

The IMF mission chief mentioned a targeted deficit at 3.5 percent of GDP in 2020.

The full text of the statement is reproduced below.

Last Friday, the International Monetary Fund (IMF) and Government of Sri Lanka (B1 stable) announced a staff-level agreement on a $1.5 billion three-year Extended Fund Facility program. The IMF financial assistance program aims to provide liquidity and support Sri Lanka’s foreign-exchange reserves and government credit metrics. The IMF program will have a credit-positive effect on liquidity, but will only marginally affect government credit metrics, unless fiscal policy implementation is much smoother than we expect. The IMF agreement comes as Sri Lanka’s sovereign credit quality is increasingly under pressure from its large fiscal deficits, high debt levels, poor debt affordability and low foreign exchange reserves.

The IMF program has three potential benefits for Sri Lanka’s external financing profile.

First, program disbursements, together with $650 million of forthcoming multilateral and bilateral loans, according to the IMF, will increase liquidity. Foreign exchange reserves have fallen to low levels relative to external debt repayments and net import payments. In the fourth-quarter of 2015, short-term external debt totalled 103.7% of foreign exchange reserves. Meanwhile, Sri Lanka’s current account deficit was 2.4% of GDP in 2015, only partly covered by foreign direct investment inflows, which also weighs on reserves. Program funding will likely reverse the decline in foreign exchange reserves and reduce Sri Lanka’s vulnerability to a sudden stop in capital inflows.

Second, the IMF financing will be at more favourable terms than Sri Lanka can get through the market. In 2015, interest payments on government debt absorbed 35% of Sri Lanka’s government revenues. As a result, the government’s fiscal metrics are very sensitive to effective interest rates. The interest rate charged on the IMF’s Extended Fund Facility programs is the Special Drawing Rights lending rate, currently 0.05% plus 100 basis points, versus the 11.75% yield on the government’s three-year notes auctioned in April.

Third, the agreement may help restore market access. The government will still rely on market financing to cover large financing needs, which the IMF estimates at 28.7% of GDP this year. Moreover, evidence of macroeconomic policy reforms, particularly regarding fiscal policy, would likely support more stable private external inflows, such as foreign direct investment. Reforms of the tax structure, collection and administration will be bolstered by the IMF’s technical assistance and credibility. On the day of the agreement announcement, the government confirmed some tax increases, including raising the value-added tax (VAT) rate to 15% and a broadening of the VAT base starting on 2 May.

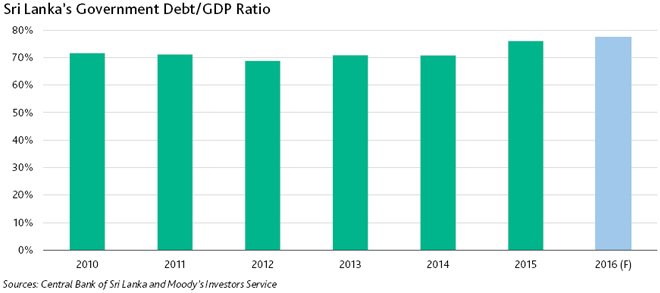

However, we expect bumps in the sovereign’s fiscal consolidation path because of difficulties in implementing robust revenue raising measures. We forecast a further increase in the government’s debt burden and debt/GDP ratio this year and next, leaving Sri Lanka vulnerable to a shift in financing conditions (see exhibit).

buy synthroid online

buy synthroid online no prescription

The budget deficit widened markedly last year to 7.4% of GDP, compared with 4.4% targeted in the budget. At 76% of GDP, government debt was high compared with similarly rated sovereigns.

The IMF mission chief mentioned a targeted deficit at 3.5% of GDP in 2020. According to our estimates, Sri Lanka’s narrowest deficit since 1998 was 5.4% of GDP in 2013. With slower growth in the next few years, and signs of financial stress for some state-owned enterprises, achieving significant fiscal consolidation will be challenging.