By Ashini Samarasinghe

Where economic performance is concerned, Sri Lanka tends to emphasize on the importance of economic growth or GDP growth over other economic indicators. This has led to expectations of consistently higher growth rates over time. However, we have not as yet been able to maintain high growth rates over a long period of time as the economy tends to experience a slowdown (what is called “economic adjustments”) from time to time.

We are experiencing a somewhat similar situation/adjustment presently. In the past one to two years we saw demand conditions in the economy improving substantially, particularly due to the low interest rate environment. The surge in non-oil imports such as vehicles and food items seen recently is a good indicator of this. The build-up of unsustainable demand conditions is now exerting pressure on the broader economy, calling for adjustments in macroeconomic variables such as interest rates and exchange rate which will eventually lead to a slowdown in economic growth.

The flip side is that such periods of adjustment are not unusual and even countries that have been viewed as having very successful growth stories in the past have had to deal with sharp downturns/adjustments along the way.

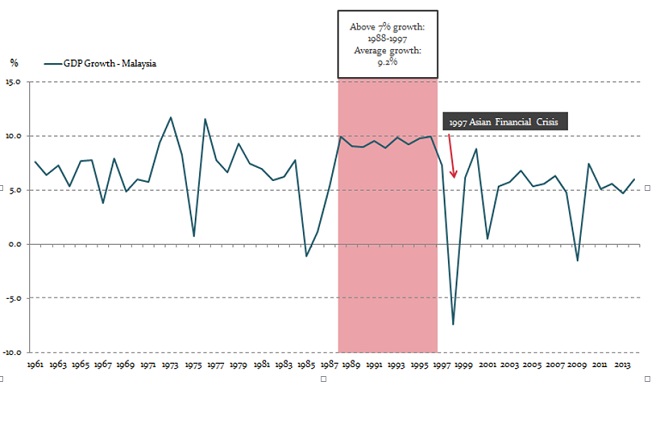

Based on a study we did on economic growth cycles, we see that a sharp slowdown in economic growth or an even worse total economic meltdown after a period of rapid growth most often seems to be a “Rite of Passage” in the Economic growth stories of most countries. This includes most Asian economies like Malaysia that Sri Lanka aspires to emulate. Here we present some key findings from a study focused on other countries’ experiences on what seems to be an inevitable cycle in economic growth.

Key Findings

Most economies that have seen a period of strong growth in excess of 7% over a period of at least 5 years has seen a crash or a major economic downturn afterwards. This is a common phenomenon even among more developed, high income countries like Japan. Singapore is a classic case in question as after every 9-10 years of over 7% growth the country has experienced a slowdown/recession.

Apart from the rapid growth in the period before, other economic issues seen in common were high current account deficits and/or a transformational “story” that attracted speculative investment and caused a real estate boom and/or construction boom often as a result of public investments (public investment on infrastructure to encourage more foreign/private investments in the domestic industrialization process) and/or accumulation of short-term external debt which ultimately drags the economy to a debt overhang.

If the challenge was a full scale Economic crisis, it was usually triggered by an exogenous/external shock which could not be dealt with due to domestic vulnerabilities of an economy as mentioned above. What usually happens is such external shocks expose the economic vulnerabilities of an economy leading to a sharp drop in FDIs and reversal of hot money flows which the country enjoyed during its high-growth era.

For instance, 1973 oil shock brought attention to Brazil’s burgeoning current account deficit which saw the economy spiraling into a debt crisis in 1982, and the 1997 Asian Financial Crisis highlighted the inefficient management of Indonesia’s liberalized capital account eventually dragging the country into an economic crisis.

A less pronounced slowdown in growth is most often caused by internal factors such as a contraction in a dominant industry like construction (e.g. Singapore 1984, Botswana 1989). In the case of Japan, the slowdown was mostly due to a maturing economy.

It is difficult to find a country which has avoided such a boom-bust cycle in economic growth. Most countries slow down after a five year period of above 7% growth (Israel, Hong Kong, Oman). A few countries have sustained rapid growth beyond five years (Singapore, Japan, Brazil, Malaysia, Indonesia, Thailand, Gabon) but have rarely gone beyond ten years.

Botswana is the exception to this which enjoyed rapid growth for over two decades (22 years, even through external crisis periods such as 1973 oil shock) before experiencing a slowdown (not a crash). However, Botswana’s growth was mainly driven by natural resources. The country possesses large deposits of diamonds and earnings from the diamond industry have fueled the country’s growth story so far. Nevertheless, sound economic policies and institutions have contributed by ensuring the productive investment of diamond earnings.

This is in contrast to Gabon which also enjoys the advantage of natural resources (oil) but nevertheless has been unable to sustain rapid growth due to inefficiencies in investment decisions.

The idea that some countries can see sustained strong economic growth for very long periods is pretty much a myth in reality. Sri Lanka is no exception to this. Thus, expectations of maintaining high economic growth rates over a long period of time may prove to be unrealistic.

(- Ashini Samarasinghe is a Research Economist at Frontier Research responsible for economic modeling and macro-economic forecasting. She also covers thematic research such as gold price movements, household income, expenditure movements and money supply & liquidity -)