Jun 24, 2020 (LBO) – Sri Lanka’s stressed external liquidity position is set to remain a weakness for the country’s credit profile, says Fitch Ratings.

According to Fitch Ratings, policymakers may be able to offer more clarity about their economic agenda once elections are held on 5 August, but hurdles to accessing additional external financing support will persist.

Full statement

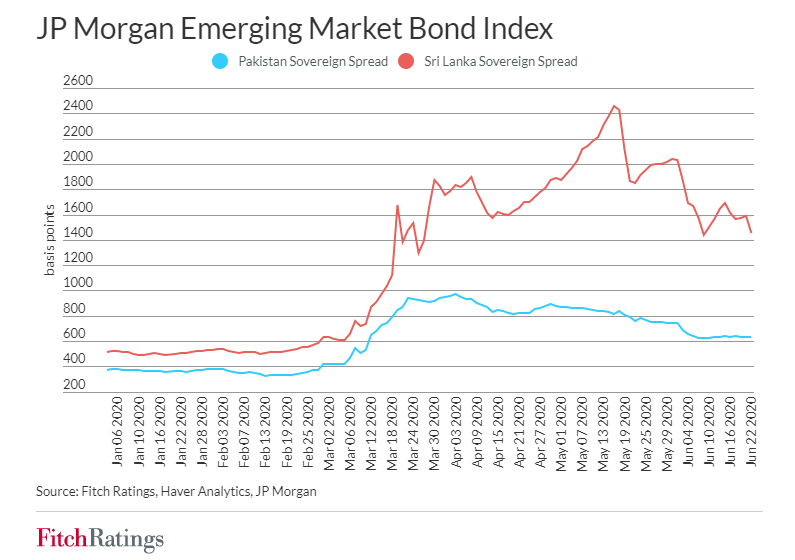

We highlighted Sri Lanka’s external financing challenges when we downgraded the sovereign’s rating to ‘B-’ from ‘B’, with a Negative Outlook, in April 2020. The country’s external liquidity ratio (defined by Fitch as liquid external assets as a percentage of liquid external liabilities), at around 60% in 2019, is among the lowest in its rating category.

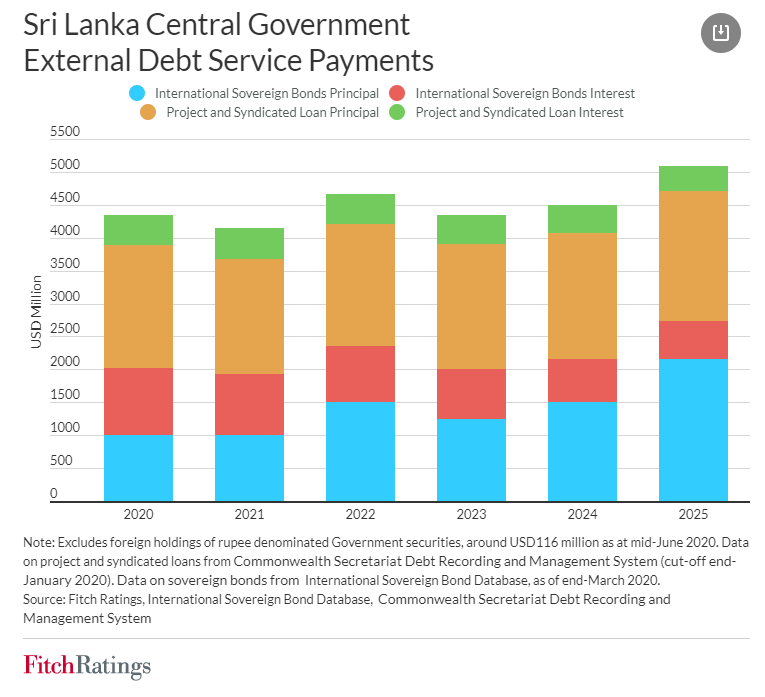

International reserves amounted to USD6.5 billion at end-May after falling by around USD716 million over the month. This level of coverage is low relative to sovereign external debt that is due the rest of this year. External debt service amounts to around USD3.8 billion from June to December 2020, including a USD1.0 billion international sovereign bond payment due in October.

Sri Lanka has yet to receive external financing from the IMF in 2020, either as part of emergency support during the coronavirus pandemic or as part of a regular programme. Greater clarity on the government’s medium-term economic policies after the elections are held could facilitate such financing, but agreeing on policies to place public finances on a consolidation path will be challenging. Sri Lanka’s recent three-year Extended Fund Facility with the IMF expired in early June after going off track last year when a new government introduced tax cuts that were contrary to the programme’s revenue-based consolidation strategy.