Tax reforms would help SL rating outlook back to stable: Moody’s

July 14, 2017 (LBO) – Evidence of effective implementation of reforms that leads to significant and lasting improvements in tax collection, and more stable external financing conditions, would support a return of Sri Lanka’s rating outlook to stable, Moody’s said.

Moody's Investors Service said signs that planned fiscal consolidation measures are less effective than Moody's currently expects or that the authorities' commitment towards such steps has diminished would weigh on Sri Lanka's rating, particularly if foreign-exchange reserves remain low while refinancing of market debt is challenging.

Moody’s, in mid last year changed Sri Lanka's rating outlook to negative from stable, with an expectation that the government's debt burden will increase further, from high levels, which could intensify external vulnerabilities and refinancing risks.

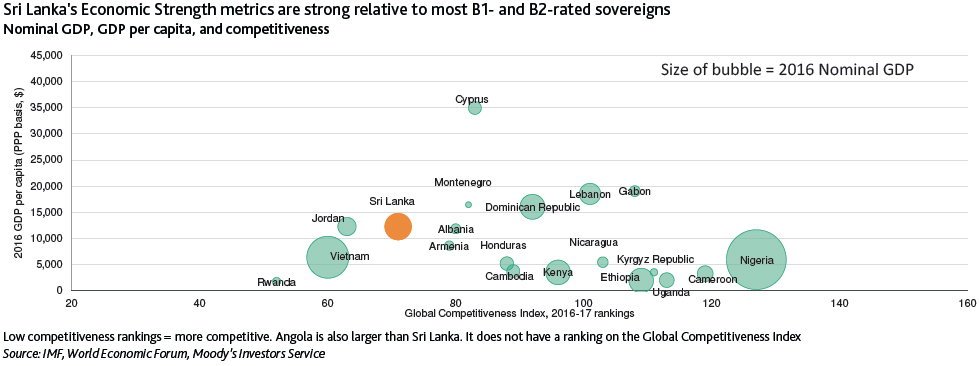

Moody's Investors Service says that the Government of Sri Lanka's B1 rating is currently supported by the economy's robust medium-term GDP growth prospects, relatively large economy, and high income levels when compared with similarly rated sovereigns.

"At the same time, despite recent progress in fiscal consolidation, credit challenges include high general government debt, very low debt affordability and large borrowing requirements. Moreover, Sri Lanka's external payments position also remains fragile," Moody's said.

Moody's conclusions are contained in its just-released annual credit analysis, "Government of Sri Lanka -- B1 Negative".

This report elaborates on Sri Lanka's credit profile in terms of Economic Strength, Moderate (+); Institutional Strength, Low (+); Fiscal Strength, Very Low (-); and Susceptibility to Event Risk, Moderate.

These are the four main analytic factors in Moody's Sovereign Bond Rating Methodology.

In 2017, Moody's expects real GDP growth of 4.6 percent, which reflects the temporary negative impact of adverse weather-related events during the first half of the year. They also expects GDP growth to average 5.2 percent per year in 2017-21, a robust growth rate.

Sri Lanka has progressed with some reforms under its three-year International Monetary Fund (IMF) Extended Fund Facility (EFF) program.

In particular, revenue measures aimed at increasing taxes, such as last year's value-added tax (VAT) rate hike and this year's pending new Inland Revenue Reform act, have the potential to sustainably increase government revenues.

"Sri Lanka's low tax efficiency and tax collection provide significant scope to broaden the tax base and increase the tax revenue/GDP ratio, which was only 12.4% in 2016," said William Foster, a Vice President and Senior Credit Officer at Moody's.

Total government revenues are also very low, with a general government revenue/GDP ratio of 14.3 percent in 2016, one of the lowest among B-rated sovereigns.

Despite ongoing fiscal consolidation, Sri Lanka's credit profile will remain constrained by its large debt burden and very low debt affordability, combined with contingent liability risks from state-owned enterprises.

Moody's expects general government debt to decline only gradually to around 78 percent of GDP in 2018, from 79.3 percent in 2016, significantly higher than the median of 53 percent for B-rated sovereigns.

Progress on reducing external vulnerability has been slower. External and foreign currency debt account for about 43 percent of total government debt, giving rise to significant exposure to external financing conditions.

In particular, large volumes of external government debt maturing in 2019-22 will test government liquidity and external vulnerability.

Further measures to build foreign-exchange reserves would help establish buffers against external pressure, in particular ahead of 2019.