Oil Equilibrium: Why Global Energy Prices Could Redefine Sri Lanka’s Economic Future

By Dr. Gayan Gunewardana (MBA, CIMA/CGMA, FRM/ GAP, AIB) & Y.K Sajani Harishchandra (MBA, ACA)

1. Introduction: When Oil Moves, Economies Shift

In the modern global economy, oil is more than a commodity; it is a macroeconomic force that shapes inflation, trade balances, fiscal stability, and the pace of global growth. For Sri Lanka, the stakes are even higher. As a country that depends heavily on imported petroleum for transport, electricity generation, and industrial activity, fluctuations in global oil markets have repeatedly triggered economic and social disruptions. Periods of supply shortages have affected daily life, strained public services, and even contributed to political instability. According to the Central Bank of Sri Lanka, the nation’s annual petroleum import bill averages between USD 4.0 and 4.5 billion, representing roughly 4.5 to 5 percent of GDP and nearly onefifth of total imports.

With Sri Lanka currently operating under an IMF program, maintaining discipline across key financial parameters — including GDP growth, currentaccount improvements, fiscal consolidation, and inflation control — has become essential. Yet none of these targets are insulated from global oilprice volatility. Understanding how oil prices interact with global and domestic economic indicators is, therefore, critical. The following analysis examines twenty years of data to uncover patterns, correlations, and vulnerabilities, and to assess how future oilprice scenarios — USD 100, USD 150, and USD 200 — may shape Sri Lanka’s economic trajectory.

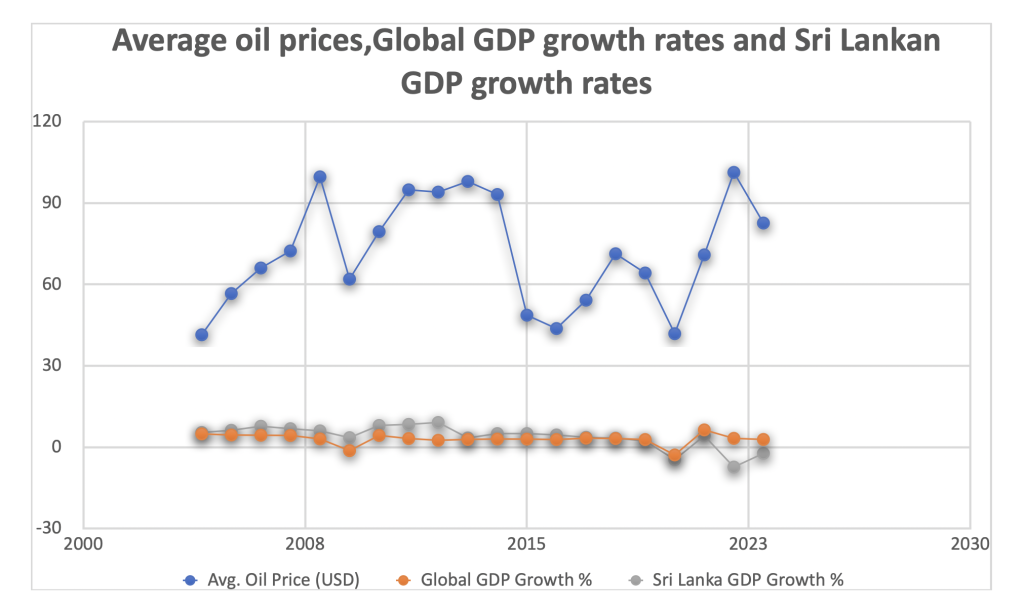

2. A 20Year Statistical Lens: Oil, Growth, and Inflation

The table below consolidates two decades of global and Sri Lankan macroeconomic indicators, including average oil prices, global GDP growth, global inflation, Sri Lanka’s GDP growth, and Sri Lanka’s inflation. This dataset forms the foundation for understanding longterm correlations and structural vulnerabilities.

20Year Statistical Summary (2004–2023)

(Sources: World Bank, IMF, Macrotrends, CBSL)

3. What the Correlations Reveal

The longterm relationship between oil prices and global GDP growth shows a weak but noticeable positive correlation. When the global economy expands, energy demand rises, and oil prices tend to follow. However, this relationship is often distorted by supplyside shocks such as geopolitical tensions, OPEC decisions, and global crises. Once outlier years like 2008, 2020, and 2022 are removed, the underlying pattern becomes clearer: global GDP and oil prices generally move in the same direction, reflecting the central role of energy demand in global production and trade.

For Sri Lanka, the correlation behaves very differently. After removing domestic outliers — years shaped by political instability, weak governance, or policy misalignment — the relationship between oil prices and Sri Lanka’s GDP growth becomes moderately negative. Higher oil prices increase the import bill, weaken the currency, elevate inflation, and reduce disposable income, all of which suppress economic activity. Unlike advanced economies that can absorb energy shocks through diversified production and financial buffers, Sri Lanka’s growth is highly sensitive to external price movements. Rising oil prices therefore represent a direct drag on domestic economic performance.

4. The MultiLayered Impact of Rising Oil Prices on Sri Lanka

The consequences of rising oil prices extend far beyond the immediate cost of fuel. Limited supply has repeatedly disrupted daily life, forcing long queues, rationing, and even midweek operational holidays in key sectors. These disruptions reduce productivity, weaken public confidence, and create ripple effects across the economy.

Industries that rely heavily on energy — including tourism, agriculture, manufacturing, and services — face rising operational costs that erode competitiveness. Tourism becomes more expensive due to higher airline and transport costs, while agriculture suffers from fertilizer scarcity and increased fuel requirements for machinery and logistics. Food supply chains become strained, pushing prices higher and intensifying inflationary pressure on households.

The fiscal and external sectors face equally severe challenges. A higher oil import bill widens the trade deficit, strains foreignexchange reserves, and forces the government to divert scarce funds toward fuel purchases. This reduces the fiscal space available for capital expenditure, including the infrastructure development urgently needed after the Ditwah disaster.

Geopolitical tensions in the Middle East add another layer of vulnerability. The region accounts for the majority of Sri Lanka’s foreign worker remittances, which have averaged nearly USD 7 billion per year over the last three years. Any slowdown in regional economic activity or disruptions to labour markets could significantly reduce this vital inflow. Tourism, too, faces both direct and indirect setbacks, as fewer visitors from the region, higher airline operating costs, and a general global slowdown reduce arrivals and revenue.

5. Strategic Responses: How Sri Lanka Can Navigate the Oil Shock

Managing the risks associated with rising oil prices requires a multipronged strategy. Sri Lanka must diversify its energy sources and explore temporary procurement arrangements from alternative suppliers, including opportunities created by recent geopolitical shifts such as the easing of restrictions on Russian oil transactions. At the same time, the country must prioritize essential sectors and implement targeted demandmanagement measures to reduce nonessential fuel consumption without undermining economic activity.

Strengthening forecasting and riskmanagement capabilities is equally important. By developing the institutional capacity to enter oil futures and hedging contracts, Sri Lanka can lock in predictable prices and reduce exposure to sudden spikes. Many energydependent economies use such tools to stabilize their import bills, and Sri Lanka could benefit from adopting similar practices under proper governance and expert oversight.

Beyond energy management, Sri Lanka must leverage its geopolitical neutrality and strategic location to attract new economic opportunities. The country’s ports, airports, and logistics infrastructure can be positioned as neutral hubs for regional trade, aviation, and maritime services. The Colombo Port City offers potential to develop a financial and services hub capable of attracting foreign direct investment from countries seeking stable, nonaligned jurisdictions. Agriculture, too, can be revitalized through targeted investment and exportoriented value chains, reducing foodimport dependence and strengthening rural incomes.

6. Conclusion: Oil Will Shape Sri Lanka’s Next Decade

Oilprice volatility is not a temporary inconvenience; it is a structural risk that will shape Sri Lanka’s economic future. Whether crude stabilizes at USD 100, climbs to USD 150, or surges to USD 200, each scenario carries profound implications for growth, inflation, remittances, tourism, and fiscal stability. Sri Lanka’s path forward requires energy diversification, stronger forecasting and hedging, strategic neutrality, investmentdriven growth, and a resilient external sector. If managed wisely, the country can transform global uncertainty into opportunity and reposition itself as a stable, neutral, and strategically located economic hub in a rapidly changing world.