Import Price Shocks of the Hormuz Crisis 2026: How Will This Affect Sri Lanka?

Dr Asanka Wijesinghe, Research Fellow, Institute of Policy Studies of Sri Lanka

- The supply shock in the commodity market directly affects 39.3% of imports of Sri Lanka, or USD 8.3 Bn, across 951 products.

- The price shock extends beyond petroleum and petrochemicals to nitrogenous fertiliser, biodiesel alternatives like palm oil, and food, exerting pressure on food prices.

- Currently, price pass-through and demand management are the best options, while easing regulatory barriers, such as licensing schemes, are necessary to ensure food security.

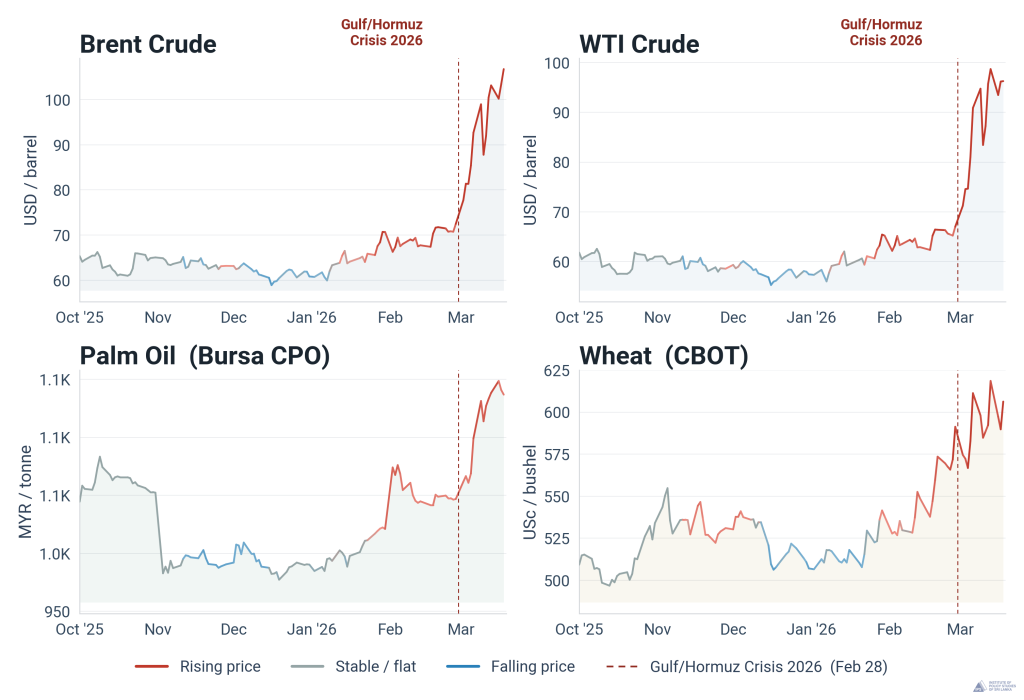

The closure of the Strait of Hormuz has unsettled global energy markets. According to the International Energy Agency (IEA), 20 Mn barrels of crude oil products were transported through the Strait in 2025, which accounted for a quarter of the world’s daily energy needs. The closure has driven fuel futures higher, with the Brent futures reaching USD 112 per barrel on 19 March 2026 (Figure 1). A phenomenon called “backwardation” is clearly visible in the fuel market, implying that spot market prices for “physical” fuel are significantly higher than futures prices for “paper” fuel.

The economic impact of the energy price shock can impact Sri Lanka through various channels, and if hostilities in oil-producing regions continue, the effects will intensify over time. The immediate impact stems from rising commodity markets, including not only fuel but also biodiesel feedstocks such as soybean, canola, and palm oil; petrochemicals; fertilisers that use liquefied natural gas (LNG) as a feedstock; and aluminium and base metals, which demand significant energy for smelting (Figure 1).

Against this background, this article examines the future prevalence of high fuel prices, Sri Lanka’s vulnerability, the impacts on foreign exchange outflows, and the necessary policy measures to mitigate the adverse effects.

Figure 1: Front-month commodity price futures from January 2025 to 19 March 2026

Source: Author’s illustration

High Fuel Prices and the Effects on Sri Lanka’s Import Basket

Given that a quarter of the global energy supply is disrupted, the current energy shock is unprecedented. After the Russian invasion of Ukraine, fuel prices rose above USD 100 per barrel in 2022, and they remained there for roughly 90 days. The high energy cost resulted in a high inflation episode in 2022-2023. As shown in Figure 2, by the end of 2023, energy prices had returned to and stabilised around the pre-invasion level. Notably, Russia’s share of the global energy market was about 11%, while the Hormuz crisis accounts directly for around a quarter of the global energy supply. The energy infrastructure damage so far has also been significant. Thus, high fuel prices may prevail if there is no swift resolution to the crisis. Sri Lanka should consider such a possibility.

Figure 2: Brent front-month price movement amidst the Russia-Ukraine crisis: 2022-2023

Source: Author’s illustration

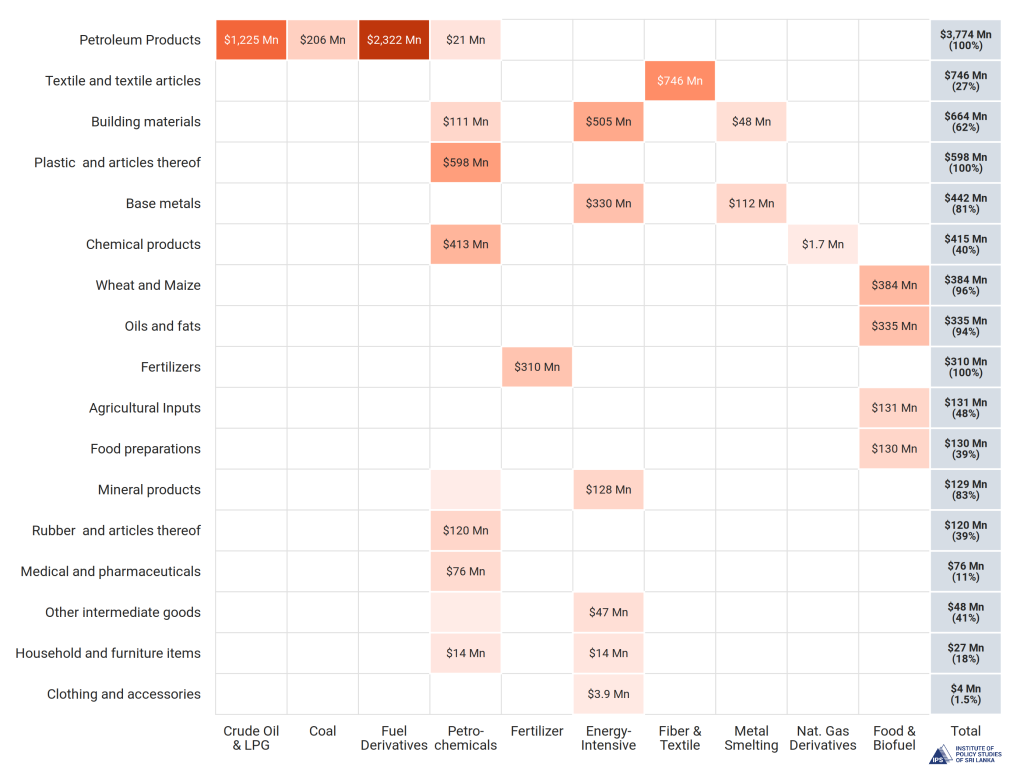

Based on 2025 import data, 39.3% of Sri Lanka’s imports, or USD 8.3 Bn, are directly exposed to rising commodity prices. Of this, USD 3.7 Bn are petroleum products, including crude oil, liquid petroleum gas (LPG) and refined fuel. Currently, the fuel price shock is 38.9% when forward-curve movements in Brent futures are factored in. Additionally, energy-intensive base metals and crude oil-based products like plastics and synthetic fibres will be expensive in the world market. These are important intermediate imports for Sri Lanka’s manufacturing sector.

Figure 3: Sri Lanka’s exposure to rallying commodity prices – base year = 2025

Source: Author

Note: The groups on the Y-axis are important import categories used by the Central Bank of Sri Lanka (CBSL). The X-axis shows the Hormuz-closure-affected product groups. At the end of the rows, the total number of affected products in the import category and the share are given. For example, 81% of base metals imports are directly affected by the rising commodity prices.

Since natural gas is a key raw material for urea, increasing urea prices, in turn, raises the costs of related agricultural commodities like wheat. As shown in Figure 3, Sri Lanka spent USD 310.1 Mn on fertiliser in 2025, while the import bill for wheat and maize was USD 384.1 Mn. The global increase in fuel prices has boosted demand for biodiesel feedstocks, putting pressure on oil and fat prices, including palm oil used for cooking. Soybean meal and maize are used in poultry feed, so price hikes will have direct nutritional effects on households, mainly through reduced protein intake.

If high prices persist, Sri Lanka’s import bill is likely to increase, as the price response can be inelastic in the short run, which is common for essential commodities with few substitutes. Using 2025 monthly import values and assuming a future fuel price shock equal to the futures market-reflected percentage increase, it is estimated that Sri Lanka’s import bill could rise by USD 1.9 Bn. This means Sri Lanka will incur a 23% increase in imports over the baseline of USD 8.3 Bn. However, the estimated value is at the upper-bound as it is assumed that Sri Lanka would consume the same quantity as in 2025. If high prices persist, adjustments across the entire economy will inevitably necessitate changes in quantity. Demand will contract when a high import price is passed on to consumers. Such a response can be quantified using product-level import demand elasticities. If higher prices lead to reduced demand, Sri Lanka’s import bill could fall by about USD 608 Mn relative to the baseline. However, such a reduction would mainly occur if energy use adjusts in line with longterm demand patterns. This estimate also does not account for wider, economywide adjustments to higher import prices. Under a full demandadjustment scenario, the overall effect would therefore be a net reduction of USD 608 Mn.

Policy Options for Sri Lanka

Although inflationary pressures remain a serious concern for Sri Lanka in the post-Hormuz crisis period, a transparent pass-through of the supply shock to price levels is a suitable policy. While memories of recent high-inflation episodes are still vivid, the Hormuz crisis and the 2022-2024 sovereign debt crises are fundamentally different events. The elevated inflation during 2022-2024 was driven by structural changes in fiscal and monetary policy. Policy implementations such as cost-reflective utility pricing, energy price pass-through, and a floating exchange rate were introduced sequentially, leading to higher inflation. The economy was moving toward reforms to address multiple distortions introduced by a low interest rate and a controlled exchange rate regime.

In the current crisis, significant price shocks from corrective policies are not anticipated. Instead, inflationary pressure resulting from the Hormuz disruption is an external, supply-side shock primarily transmitted through the prices of imported fuel, rather than via domestic policy reversals. Since high airfares and rising shipping fuel costs may impact foreign exchange inflows, managing the reserve position becomes crucial. In this context, restricting fuel consumption is essential while ensuring available fuel is allocated primarily for industrial use.

A fiscal response that suppresses the price signal, such as reducing taxes on certain imported goods, might not be suitable at the moment, as it could boost demand for very costly imported products like fuel. The analysis shows that the import bill can rise substantially if a high price prevails without a quantity adjustment. Notably, under the current framework, such import demands are transmitted to the exchange rate, which can further increase inflationary pressures. However, Sri Lanka should consider easing import licensing schemes for animal and poultry raw materials as global market prices rise, to facilitate imports and secure food supply. Temporarily removing the existing Special Commodity Levy (SCL) on corn imports should also be considered. These products incur small reserve outflows but play a larger role in the country’s protein nutrition.